The leaves are changing color, the temperatures are cooling down, so the real estate market must be starting to slow down, right? 2020 has been a year unlike any other so why should it be any surprise that the real estate market isn’t following its normal pattern either. So far, the only thing in the real estate market that has continued to slow is the number of listings that are coming on the market, causing inventory levels to fall to the lowest levels we have seen in over 5 years.

In this month’s real estate market update, we will look at the latest numbers for the overall economy then focus on the latest numbers specific to the real estate market. Will home prices continue to rise in 2021 or will there be a rise in foreclosures to cool things down. Watch the following video or continue reading below to learn more.

Latest on the Economy

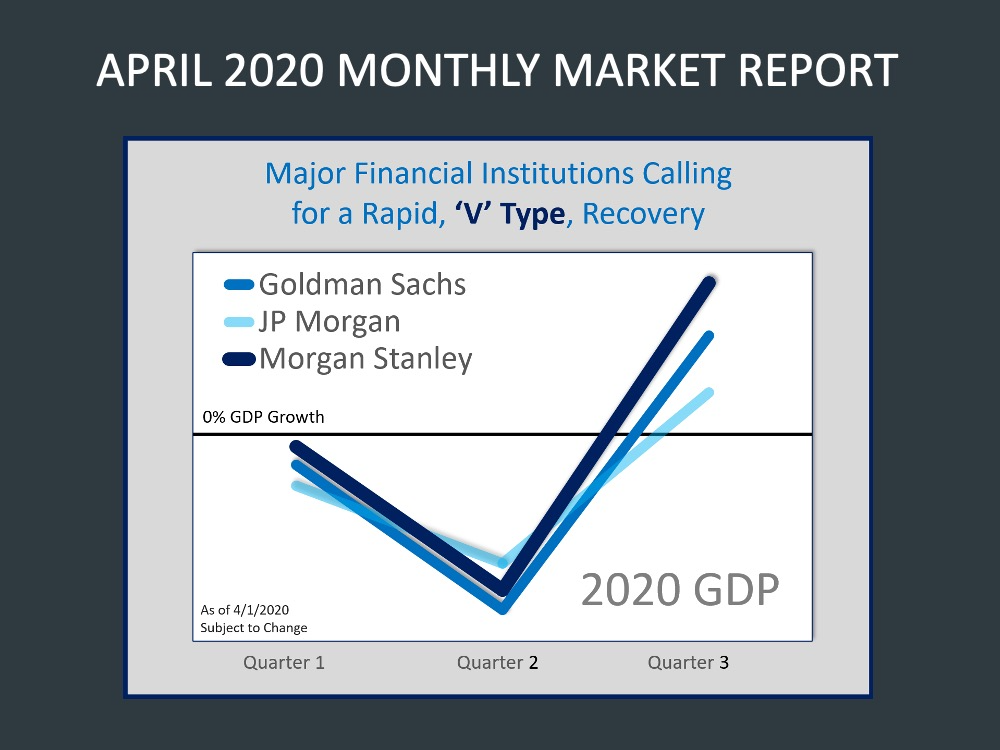

Back in April, I included a slide in my monthly real estate market report showing that major financial institutions were forecasting a strong V-shaped economic recovery. The belief was that the downturn was being caused by a health issue and not an economic one, given the underlying economy was strong going into the pandemic. As a result, the economy was projected to recover quickly. Here is that slide from April.

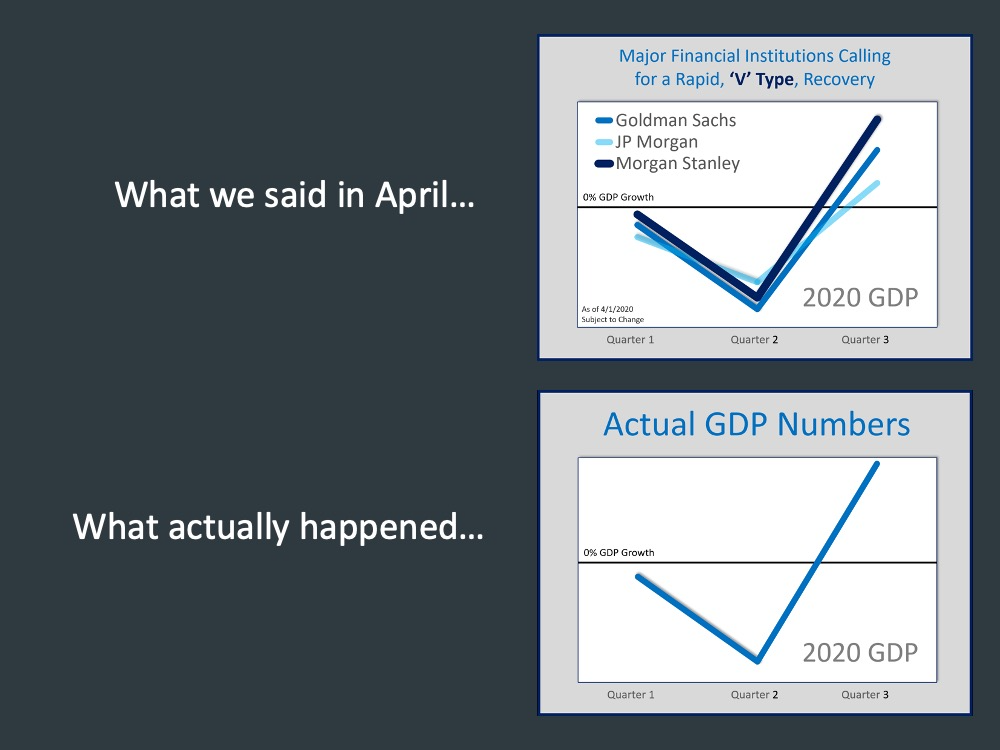

I must admit, I received some push back from several people who believed I was intentionally trying to paint an overly optimistic forecast when the April market report came out. I explained that I wasn’t trying to be optimistic, or pessimistic, just share the information I have access to and add my thoughts so that people can make the best decision for their own situation. Saying that I have to admit I couldn’t help but crack a wry smile when the latest economic data was released. Here is that same slide next to what has actually happened over the last two quarters.

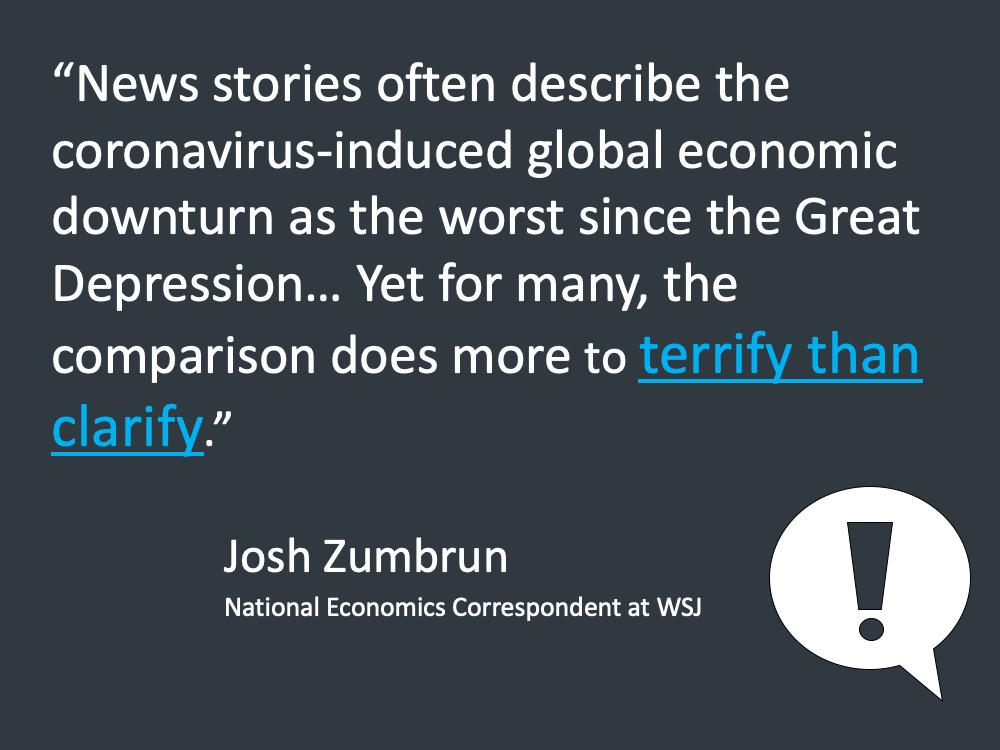

Maybe it’s just a coincidence that the two slides look virtually identical! In all honesty, the reason I share the information that I do is that it’s often different than what the media reports. Maybe I’m becoming a little more cynical as I get older, but it seems that everything we hear on TV, or read online, isn’t what it seems at all. Even Josh Zumbrum, National Economics Correspondent at the Wall Street Journal seems to hint at the fact that there is a level of sensationalism to what is being reported.

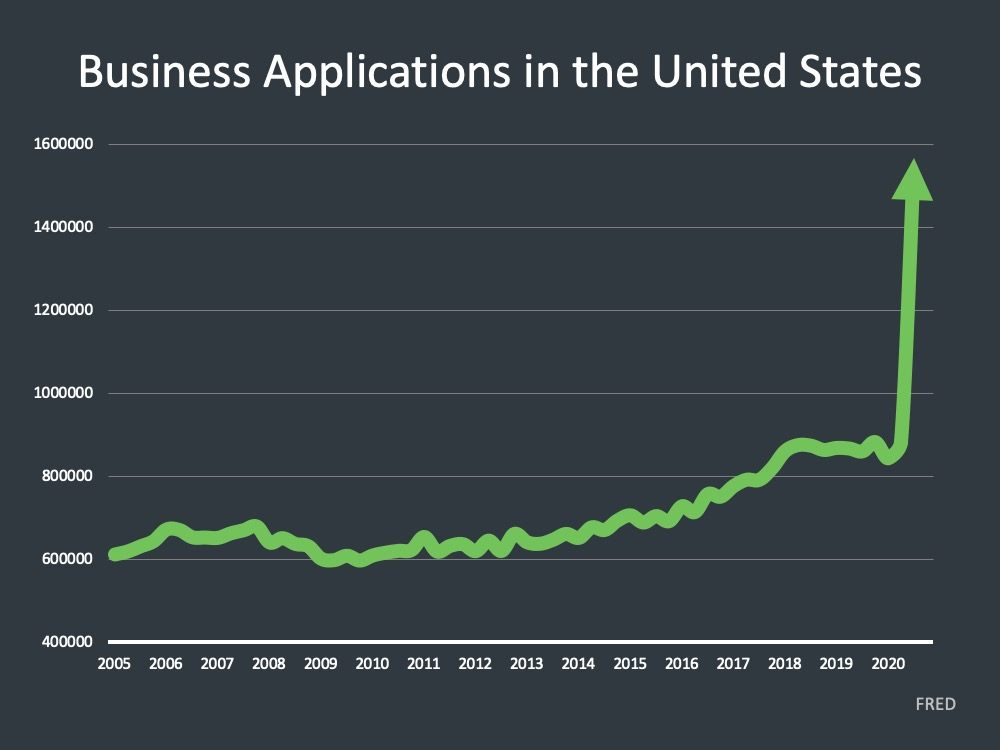

I’m not trying to downplay the fact that we have/are dealing with a serious health crisis and I know that a lot of families have been impacted not only by the virus but by the economic fallout as a result. The service and hospitality sector have born the brunt of the pain from an economic perspective, but opportunity is often born in difficult times. Some of the most successful companies of today were born during the great recession and what hasn’t been reported much is how many new businesses have been started this year.

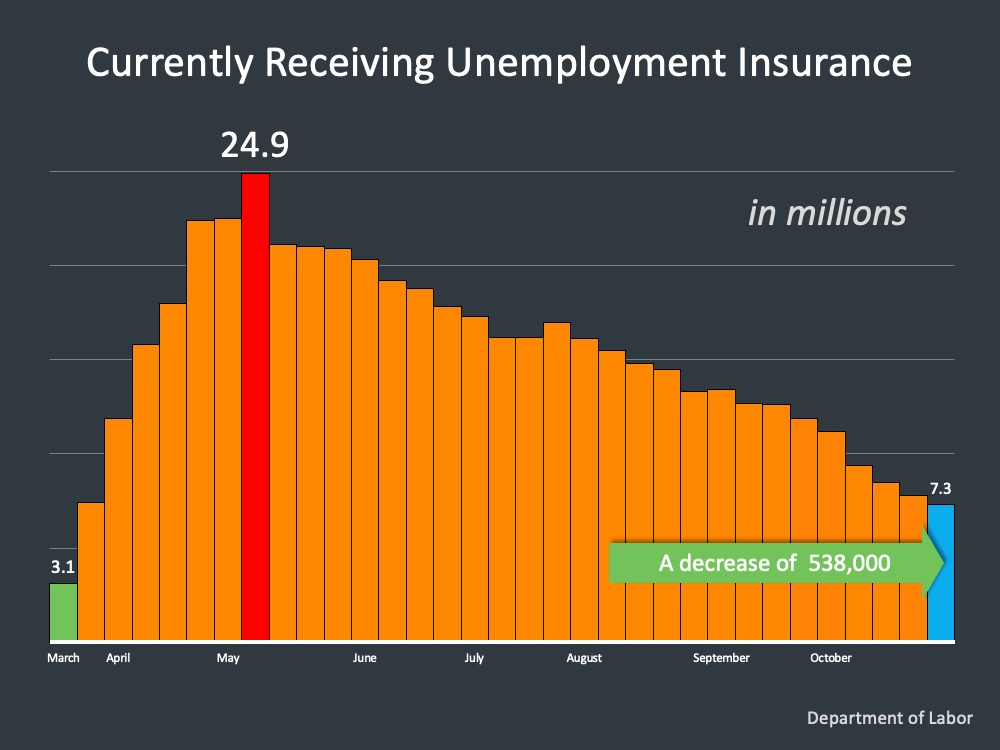

That being said, high unemployment is still something that we have and are going to be dealing with in the years ahead. While there is often a focus on new unemployment filings, which is important, I have also been tracking continuing unemployment in terms of the number of people that are actually receiving unemployment insurance. That number, which reached 24.9 million in May 2020, fell by an additional 538,000 to 7.3 million continuing claims.

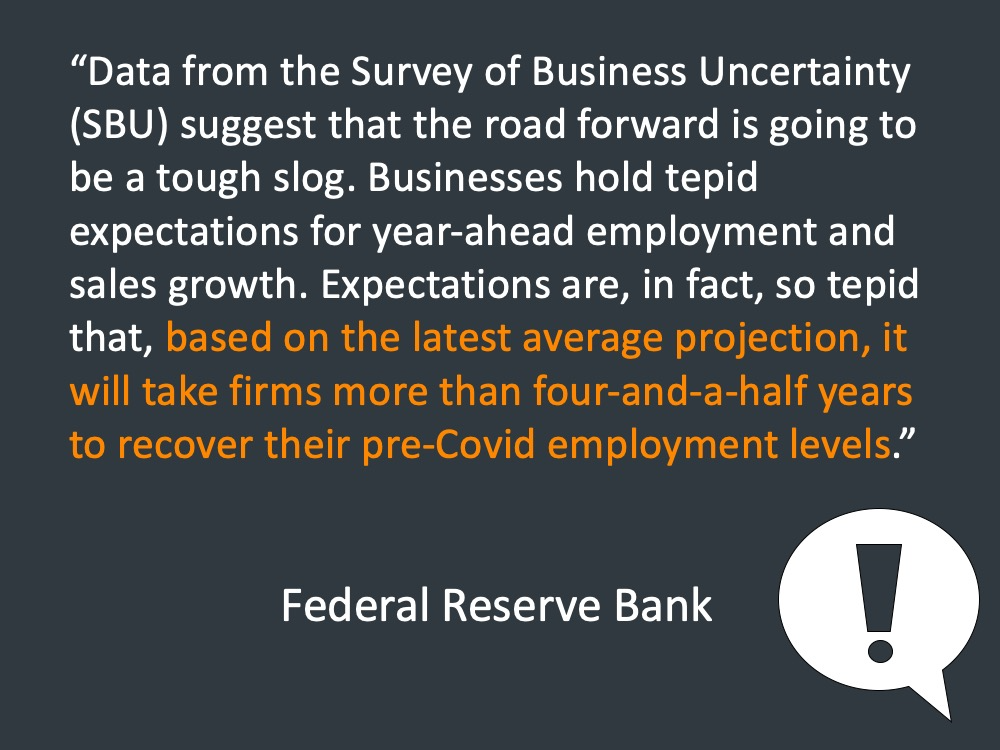

The fact that unemployment numbers continue to fall and new businesses are being created is great news, we still have a long road ahead and there remains a great deal of uncertainty. This was echoed in a recent statement from the Federal Reserve.

What About Mortgage Forbearances and Foreclosures

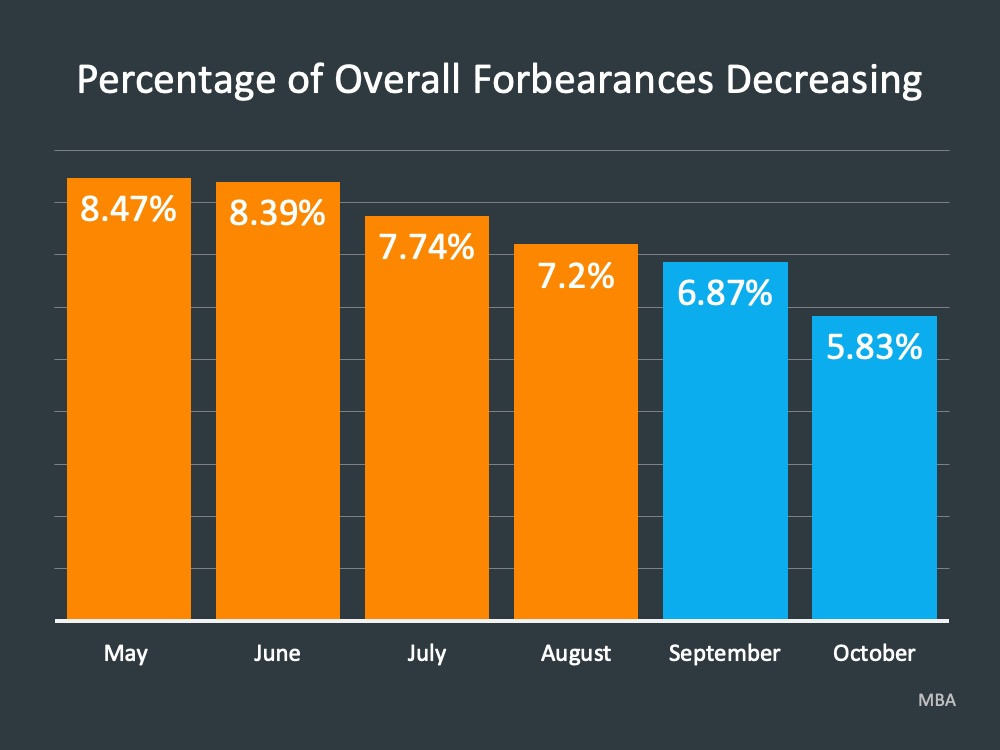

When the unemployment numbers spiked, a number of families were left wondering how they were going to pay their bills, including their mortgage. One of the early mitigation efforts was mortgage forbearances, which allow you to defer mortgage payments for a period of time. Initially, those payments were deferred for 90 days with a lump sum of all missed payments due at the end of that time period. Many were quick to say this would lead to a flood of new foreclosures and cause a housing market crash. The initial 90 day forbearance period was put in place to give everyone a little time to breathe and figure out what’s next. Having been through the last foreclosure crisis I knew the last thing the banks wanted was to go through that again. Like unemployment, the forbearances numbers also continue to improve as shown on the following slide.

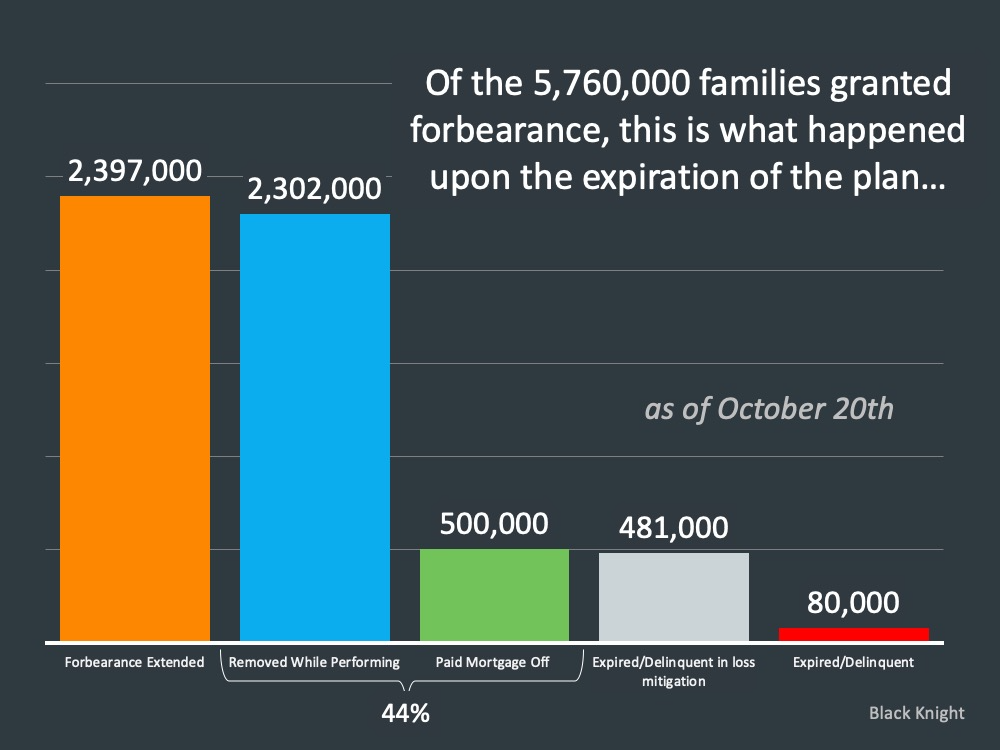

As expected, at the end of the initial 90 days new mitigation efforts were put in place and the Cares Act also introduced new measures to make sure people were not being forced from their homes. Of the 5.76 million families that originally entered a forbearance plan, 44% have either brought their loan current or paid off the loan, most likely by selling the property. The number actually in foreclosure is relatively small and definitely not amounting to a coming wave of foreclosures as some predicted.

The Outlook for Home Prices

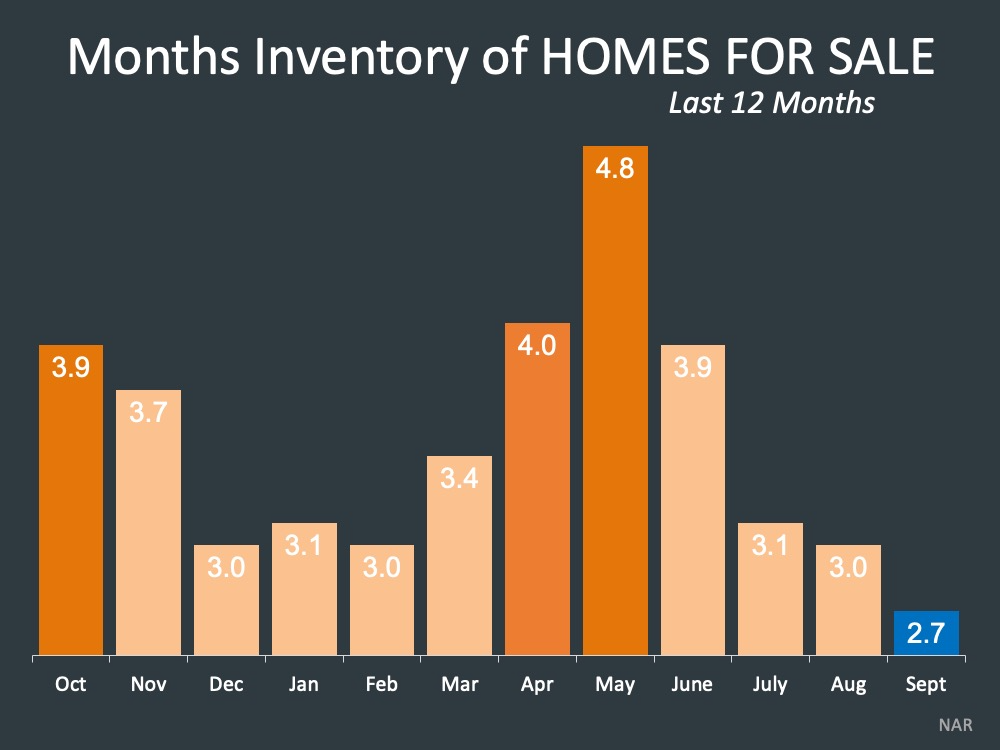

Unlike when the real estate market crashed in 2007/2008. home prices today are playing nice with the law of supply and demand. Supply has been relatively low for the past year and has only continued to fall. If nothing else, the pandemic has made many people realize that their current house no longer suits their needs either in terms of size or location. The reality of more and more people working from home is something that appears will be with us for quite some time. Those changing requirements, coupled with record low interest rates, have continued to fuel housing demand. Uncertainty on where everything is heading, however, has caused many would-be sellers to hold off putting their home on the market. A recent Zillow survey confirmed this as 34% of potential sellers said general uncertainty has caused them to delay their plans to sell. As a result, inventory levels continue to fall.

Keep in mind that 6 months worth of inventory is considered a “balanced” market. In the markets that my team operates in inventory levels are even lower than the national average.

In Frisco, TX inventory is down 62% year-over-year to a 1.4 month supply

In Proser, TX inventory is down 75.6% year-over-year to a 1 month supply

In Temecula, CA inventory is down 37% year-over-year to a 1.7 month supply

This is the lowest inventory has been in all of these cities in the past 5 years.

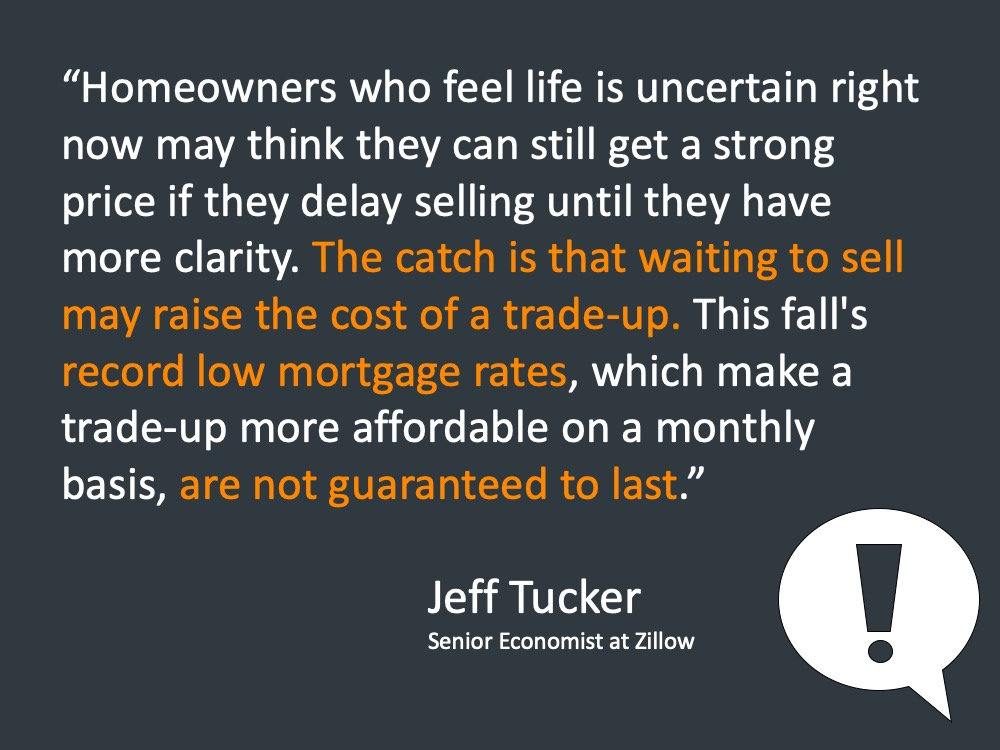

As with anything, there is an opportunity cost when decisions are delayed. While home prices do continue to rise, homeowners who have delayed putting their home on the market due to uncertainty may find that the cost of their next move is also going up.

The point here is that if someone is considering selling and moving to a larger home, the home they are wanting to move into is going up exponentially more than the home they currently live in. For example, if you currently live in a home worth $400k and the home you want to move to costs $600k, if prices go up 10% in the next year you will be able to sell for $440k, but the home you are hoping to buy now costs $660k.

Obviously, the opposite is true if you are looking to downsize. Everyone’s situation is different. It is a matter of taking the information available and making the best decision for you.

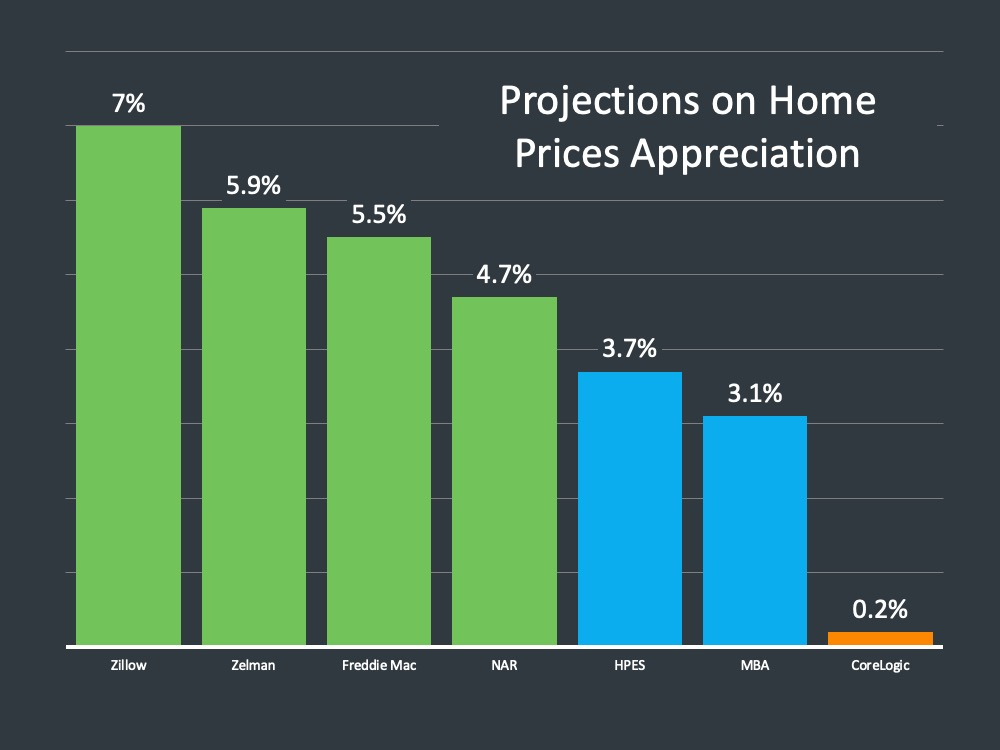

With demand being high and supply being low it should come as no surprise that home prices are expected to continue increasing over the next 12 months. The experts agree and this is expected to hold true regardless of the ultimate outcome of the election. Here is what the latest forecasts are projecting.

Almost all of these forecasts have been revised up in the past couple of months. Even though CoreLogic is only forecasting a 0.6%gain, I should point out that they were previously forecasting a 6.6% decline.

As a comparison to these forecasts, the median home price in Frisco, TX is up 5.4% year-over-year, in Prosper, TX it’s up 11.3% year-over-year and it’s up 14.1% year-over-year in Temecula, CA.

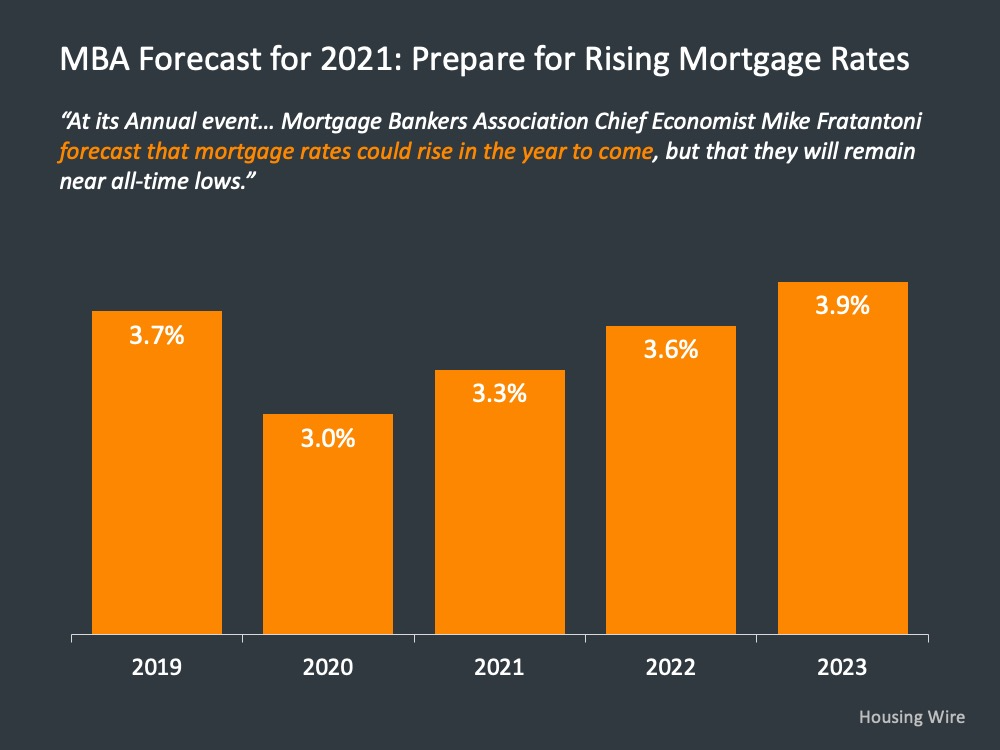

Mortgage rates, which have undoubtedly played a major role in increased demand are not expected to stay this low forever. While the forecast increase is not dramatic, I want to point out that a 1% increase in the mortgage rate, decreases your purchasing power by 10%.

If home prices were to increase 5% per year for 3 years and mortgage rates go up 1% in the same time period, the house you are looking at today would essentially be 25% more expensive 3 years from now.

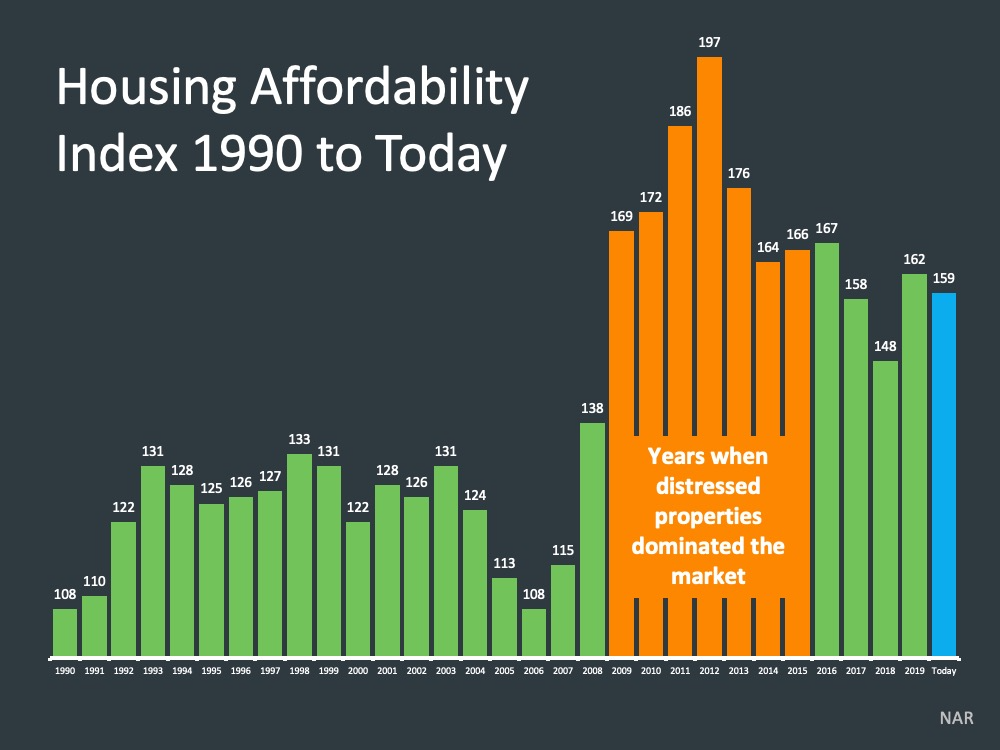

The important thing to point out on the slide above is that the higher the number you see, the more affordable housing is. Although housing has remained affordable, the pace of appreciation might have finally caught up with the record low-interest rates.

Market Dynamics

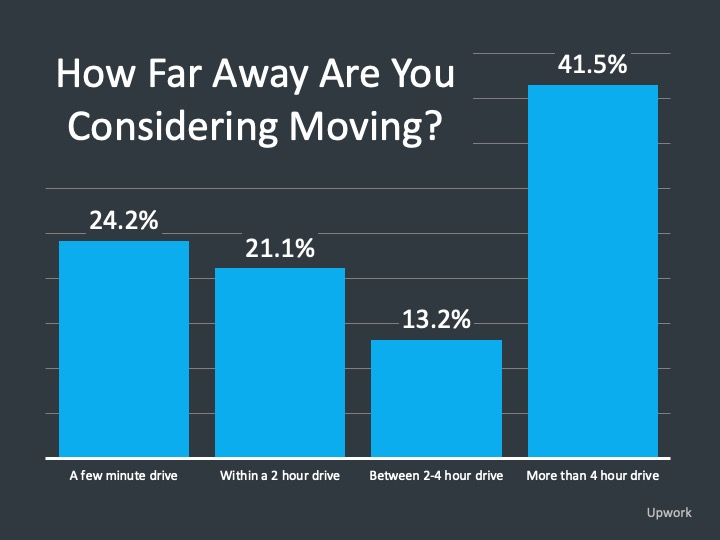

The last point I want to touch on in this update is the potential change in housing market dynamics. It is becoming more and more apparent that there is a shift underway from large corporate campuses to smaller facilities with more employees working remotely. People have primarily tended to live close to the cities within a reasonable commute time from the office. If you take that away everything changes. Families living in cities are starting to move further into the suburbs for more space, more house, and better quality of life. I had a real estate associate on Maui tell me they were seeing an influx of home buyers from Silicon Valley as many tech engineers were now being able to work from anywhere. This was confirmed in a recent survey of potential home buyer by Upwork who asked how far away people were considering moving.

Bottom Line

As mentioned above, everyones situation is different and only you can make the decision that’s right for you and your family.

If you’ve been thinking of making a move, but aren’t sure if this is the right time for you, please feel free to Schedule a Call with me. I’m happy to share the information I have and hopefully provide some insights that will help you make the right decision for you.