I saw a headline the other day that asked “Will the real estate market ever get back to normal?”

It’s a great question, isn’t it? Life has been anything but “normal” the past two years and the real estate market has been no exception with high demand, low supply, rising prices, and frustration all around.

There are signs the frenzy is cooling and more typical seasonal patterns are starting to return. Continue reading below, or watch the following video, to learn more about what I expect we will see going forward.

In a typical year, the real estate market follows a very predictable pattern. Inventory is lowest at the beginning of the year following the holidays, new property listings and activity pick up rapidly through the spring, peaking in May/June, before starting to fall off again over the summer and into fall.

In 2020, that typical pattern was broken by the pandemic and resulting lockdowns. In what should have been the busiest time of the year for real estate there was virtually no real estate activity at all. Rather than losing that activity, as many predicted, it simply shifted to later in the year. Spring activity shifted to summer and summer to fall, almost as though the pause button was pressed as once we hit play again things picked up right where they had left off. Rather than diminish, demand for housing soared fueled by a changing definition of what home meant for many and falling mortgage rates. By February 2021, at least here in Frisco, the imbalance between supply and demand reached the breaking point as that is when the multiple offers, bidding wars, and rapidly rising prices started in earnest.

Jessica Lautz, VP of Demographics and Behavioral Insights for the National Association of Realtors (NAR) recently said:

Real estate transactions typically don’t occur because of market events, but because of life events. I’ve long said the best time for someone to buy or sell a home is when it’s the right time for them to buy or sell a home. People get married, start a family, job change, divorce, kids move out, etc.

The difference in 2020 is that the entire world had a life event. Factors that don’t typically impact housing suddenly did, which changed the definition of home for many. Home was now also your office, classroom, gym, movie theater, and vacation destination. This caused many to realize their current space no longer worked for them. The apartment, or condo, surrounded by other people wasn’t as desirable as a house in the suburbs with more space and privacy.

This changing definition of home caused more people to want to make a move sooner than we have seen in recent years.

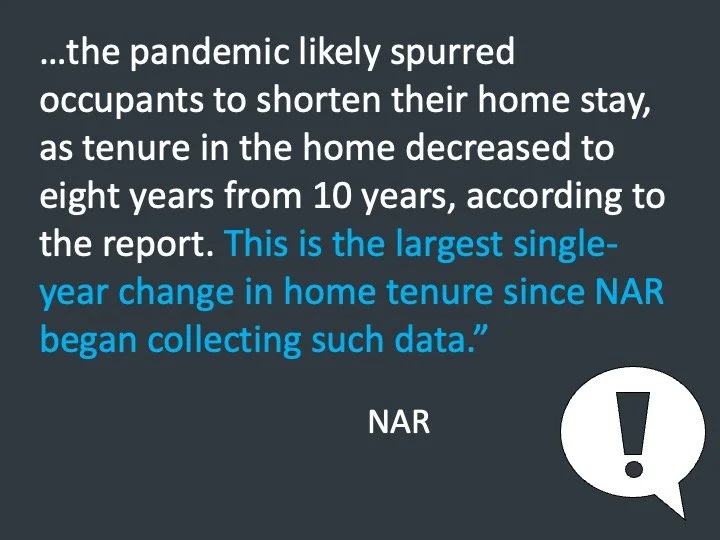

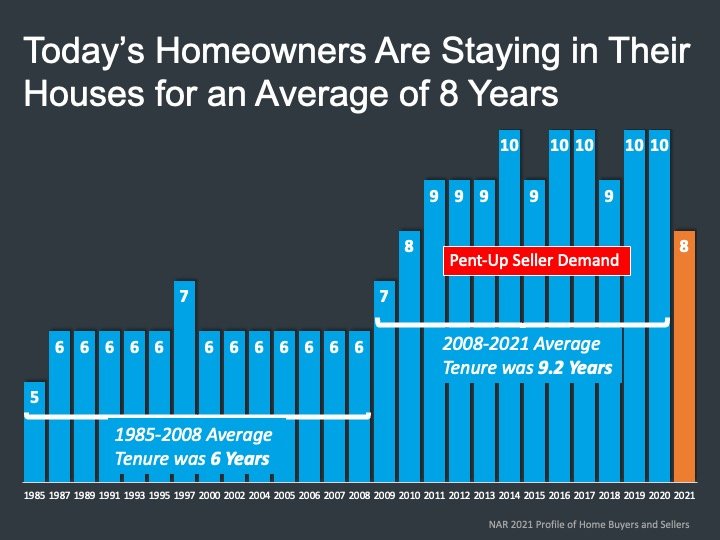

From 1985 until 2008 the average length of time someone stayed in a home before moving was 6 years. This climbed to 10 years after the real estate market crash and stayed there until this past year.

There are a couple of reasons for this;

Typically, homeowners use the equity they have built up in their current home to fund the purchase of their next home. When the housing market crashed in 2008 much of that equity was wiped out, meaning homeowners could no longer afford to make the next move.

Mortgage standards, which were very loose in the years leading up to the crash, got very tight, preventing many would-be home buyers from being able to qualify for a new mortgage.

The graph above shows that seller demand (people who want to sell) has been building since 2011 for the reasons given above. It appears as though the pandemic was the impetus that many sellers needed to go ahead and make the move.

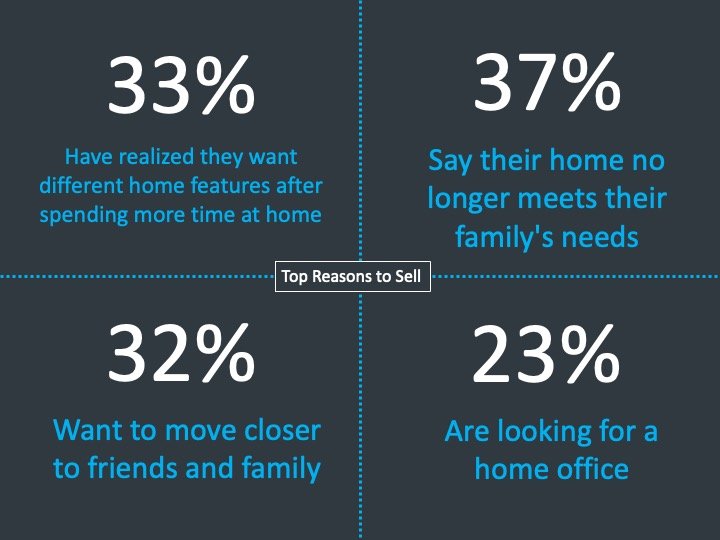

Further evidence of this can be found in the same NAR survey that asked would be sellers why they were selling;

Going Forward

One of the biggest challenges potential sellers have been facing is where will they go if they sell? As mentioned above, by early 2021 housing demand had outpaced supply to the extent that multiple offers and bidding wars became the norm. This has caused many sellers to delay selling due to the fact that they haven’t been able to find a replacement property.

Relief is most likely to come in the form of new construction. For over a decade now there haven’t been enough new homes built to satisfy demand created by new household formation and replacement of old structures. The good news is that home builders are on pace to complete 1.6 million new homes this year, the highest annual number since 2006, which will help bring supply balance back into the market.

More inventory coming to market, coupled with rising mortgage rates, will put downward pressure on home price appreciation. This won’t be immediate, but we are already seeing the pace of appreciation moderate. Year-over-year appreciation back in May/June was trending at about 18% nationally and that has dropped to 10% in the past week. I fully expect that will continue as we move into 2022. More inventory will also mean fewer bidding wars and fewer multiple offer scenarios.

Bottom Line

Market conditions remain challenging in many areas of the country, but it does appear as though we are past the height of the frenzy and on our way towards more normal conditions. As always, if you have any questions, or would like to discuss your real estate goals for the coming year, please feel free to schedule a call as I’d be more than happy to talk to you.