Just like summer temperatures, the real estate market has been red hot the past few months. Sales activity has broken records and the slowdown we usually see as we move towards fall hasn’t started yet (and might fail to show up at all). This month’s real estate market update is going to focus on three main areas;

1) Provide an overview of the latest activity

2) Share the latest information on what home prices are expected to do over the next 12 months

3) Update mortgage forbearance activity and what that could mean for foreclosures

Whether you prefer to watch or read, I’ve got you covered so click on the following video or continue reading below.

Real Estate Market Overview

As we’ve talked about in previous market updates the real estate market in 2020 started the year very strong then the pandemic hit and it was as if the pause button was pushed. Activity dropped off substantially, and suddenly, but came roaring back faster and stronger than many believed was possible.

So why has the housing market remain so strong?

Rather than stumble and stall from the uncertainty caused by the pandemic, the pandemic actually seemed to fuel people’s desire to move. This hasn’t been isolated to one particular sector either. Renters desire to own a place of their own increased, many living in cities suddenly wanted more open space and less congestion, while others, seeing that working remotely and online school were not going to be temporary situations, determined their current space didn’t meet their future needs as well as they previously thought. Regardless of the reason, people are on the move and monthly sales records continue to be broken.

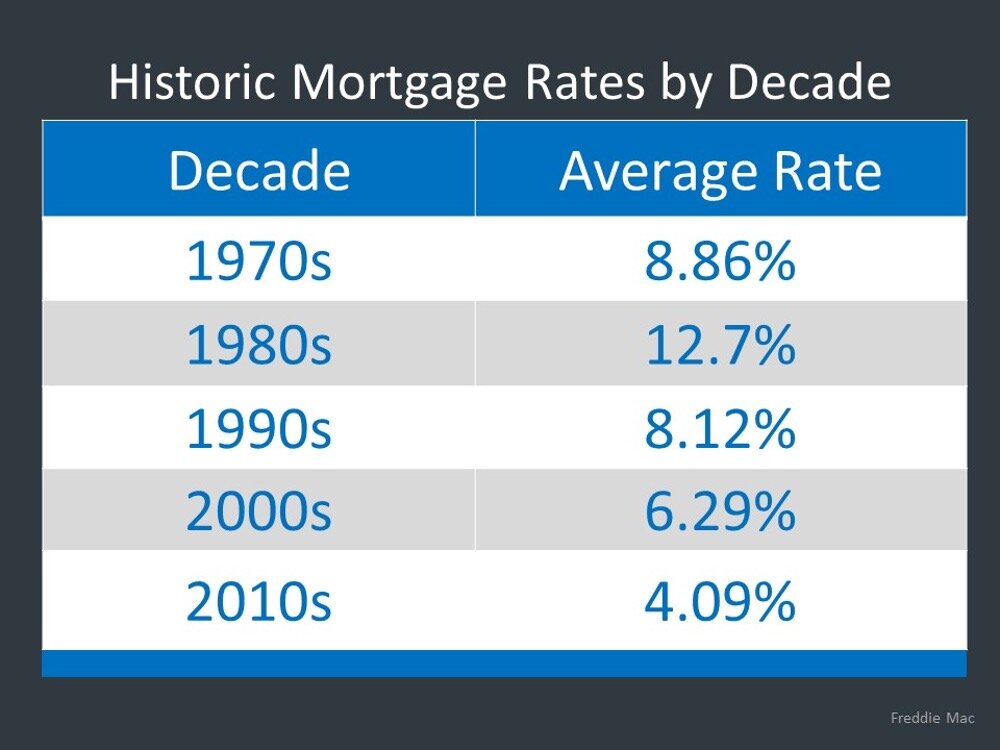

Affordability is also playing a major part as record-low interest rates are helping to make buyers plans a reality. As of writing this blog post the 30 year fixed rate mortgage stands at 2.86%, a rate that many, including myself, didn’t think we would ever see. To put this into perspective, here is what the average mortgage rate by decade has been going back to the 1970s.

We often hear the term affordability and record low mortgage rates, but don’t often have any perspective as to what that actually means. Simply put, imagine you were looking for a home last year but didn’t end up finding what you were looking for and decided to wait. Without any changes to your income, based solely on the drop in mortgage rates, you can afford approximately 10% more home this year than last. Yes, I know prices have increased, but they haven’t increased more than 10% in all areas so you get the idea.

New mortgage applications are one of the trends we look at as a leading indicator of future home sales activity. The idea is that if more people are submitting applications for a mortgage then there is a high likelihood that more people will be out shopping for a home.

Over the last 4 weeks, when looking at the week-over-week trend, the number of new mortgage applications has actually been falling slightly. I do mean slightly as we are only talking 1% to 2%, but year-over-year the number of new mortgage applications is up 25% to 30%. So why the difference? The week-over-week decline coincides with schools and fall sports starting and could also be an indicator that we are finally working through the pent-up demand that has existing since the lockdown period.

Home Price Expectations

Home prices, like all goods and services, are subject to the principle of supply and demand. As shown above, demand isn’t a problem. One of the biggest challenges in the real estate market currently is the lack of supply, just ask anyone who has been out looking for a home.

With high demand and limited supply it should be no surprise that home prices are continuing to increase. 8 of 9 institutions surveyed are all expecting home prices to increase over the next 12 months.

What is interesting is how this forecast has changed over the past few months. Initially, the general consensus was the economic uncertainty and unemployment caused by the pandemic would have a negative impact on future home prices. That obviously hasn’t happened to date and isn’t expected in the next 12 months as the graph above shows.

Here is the difference between what was forecast and what is being forecasted now.

Mortgage Forbearances and Foreclosures

When the economic shutdown first happened and unemployment skyrocketed there was widespread speculation that we were going to be facing a housing crisis like we experienced in 2007, 2008, 2009. The number of homeowners requesting help with their mortgage (forbearance) soared. The thought process was that the forbearance period would end and homeowners wouldn’t be in a position to catch-up on missed mortgage payments so a wave of foreclosures was in our future.

My take on this was “not so fast”. I firmly believed that too many people were jumping to conclusions. My reason for this thinking was that the banks learned their lesson in the housing crisis and didn’t want a repeat of that. Market conditions are vastly different now than they were in 2007, 2008 and homeowners are sitting on a lot more equity than they were back then which creates options.

The number of mortgages in active forbearance has stabilized over the past few weeks.

Please don’t get me wrong, 3.93 million mortgages in forbearance is still a large number, but that doesn’t mean that all of those homes will become distressed properties. Will there inevitably be foreclosures, yes, but I don’t see any reason to believe that a wave of foreclosures is coming like some have suggested.

One important thing to remember is that foreclosures are part of every real estate market, good and bad. To put this in perspective here is a graph showing the percentage of sales that involved distressed properties back in 2012 compared to what we are currently seeing.

The resiliency of the current housing market has been remarkable. Even with the time and sales that were lost as a result of the lockdown, it is now looking as though total home sales this year will actually exceed what we saw in 2019 and total sales in 2021 are forecast to increase between 8% and 12% according to Lawrence Yun, Chief Economist, National Association of Realtors.

Bottom Line

In a policy meeting this week the Federal Reserve stated they expect to keep interest rates near 0% until 2023. That doesn’t necessarily mean mortgage rates will remain at historically low levels as mortgage rates are tied to bond yields, but it does mean that conditions to buy a home should remain favorable.

As mentioned above, one of the biggest challenges facing the real estate market currently is the lack of inventory. If you have been considering selling and making a move now could be the ideal time.