It’s hard to believe that we are already 6 weeks into the new year. It feels like I just finished putting my Christmas decorations away!

In the real estate market, 2021 has started right where 2020 finished and there are no signs of a slow down any time soon. While one would assume a strong real estate market is a good thing, and it is for the overall economy, the current market does bring about frustration for both buyers and sellers. Buyers are tired of being outbid and homes selling as fast as they come on the market while many sellers are hesitant to list their homes for sale out of fear they won’t be able to find a replacement property and will end up with nowhere to go.

In this month’s real estate market update, I take a look at the final numbers for 2020, talk about the impact supply and demand is having on home prices, take a look at affordability, and lastly provide an update on mortgage forbearances and potential foreclosures. Check out the following video, continue reading below, or even do both! As always, if you have any questions, please don’t hesitate to reach out.

How Much Equity Did Your Home Gain in 2020?

CLICK HERE to Find Out Instantly!

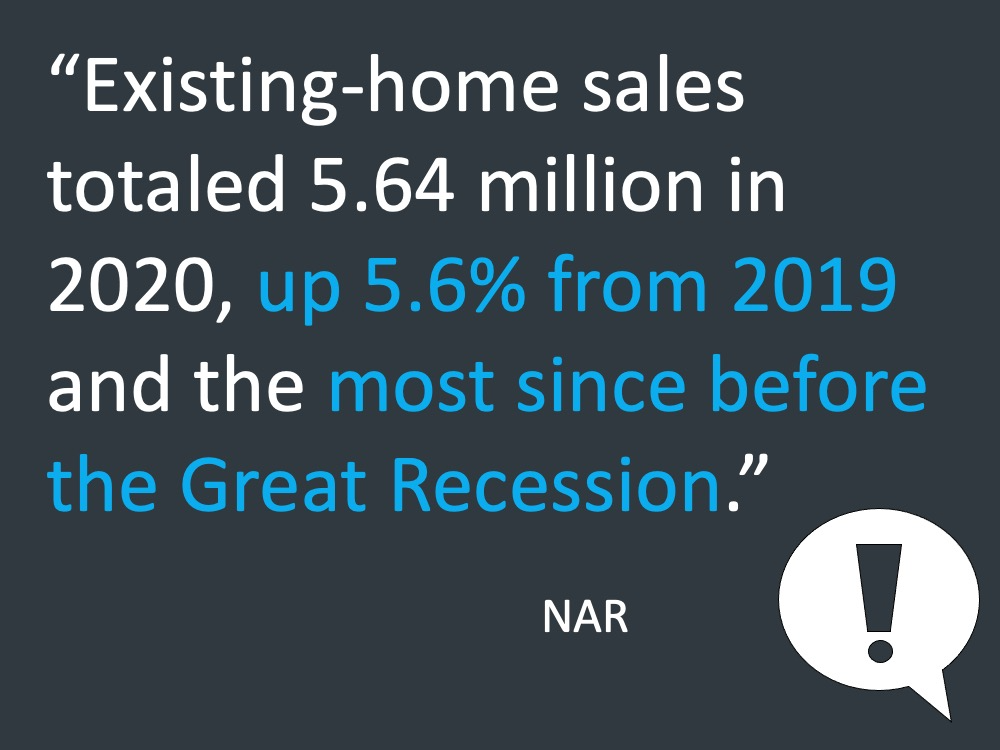

The final numbers for home sales in 2020 are in! When the pandemic started there were many that predicted rising unemployment, coupled with the health-related lockdown, would lead to a housing crisis. Instead, more homes were sold than in any year since before the Great Recession.

Home sales in 2021 are currently forecast to surpass 2020 levels. Saying that, the biggest challenge facing the real estate market currently is the lack of inventory, You can’t buy what isn’t available.

A balanced market, one that neither favors buyers or sellers, is generally achieved when there is 6 months of housing inventory available. (Months of inventory refers to the length of time it would take all homes currently listed for sale to sell at the current pace of sales.) Nationally, here is how inventory currently looks;

Inventory levels in both Frisco and Prosper are even tighter as both markets currently have less than a 1 month supply of inventory.

Home Prices

While there has been talk and speculation about a new housing bubble, I don’t believe we are approaching bubble territory at this time. Current home prices are only now reaching the heights achieved prior to the crash in many markets and when you add in the 3.8% historic annual appreciation rate, current home prices are right where they should be. Home price appreciation is currently being driven by supply and demand, not speculation. As shown above, supply is incredibly low and demand is high due to people’s changing housing needs, partly as a result of the pandemic, and historically low mortgage rates.

Nationally, home prices rose by an average of 9.2% in 2020. Year-over-year, from January 2020 to January 2021, home prices were up 15.2% in Frisco and 6.8% in Prosper. Home prices obviously cannot continue rising at that pace or we will find ourselves heading for trouble. The expectation is that we will see the pace of appreciation moderate this year.

Every market is different though and locally we can expect to see continued appreciation rates that beat the national average due to demand from population increases, but tapered appreciation compared to the last couple of years.

Affordability

Whenever there is rapid home price appreciation housing affordability always comes into question. Record low mortgage rates have helped keep affordability in check, but mortgage rates have increased in 4 of the first 6 weeks of this year. Mortgage rates are currently still below 3% and the expectation is that while mortgage rates will continue to rise, they will not rise above the low 3’s before the second half of 2022.

Wage growth is another piece of the affordability equation. While home prices have continued to increase wages have also been increasing the past several years. Historically, the median mortgage payment would require 21.2% of the median monthly wage. Today we are trending at 14.9%.

As a result, housing affordability remains higher than it has been at any time since 1990 except for a few years in the midst of the great recession as shown on the following graph: (The higher the number the more affordable housing is considered.)

What About Supply?

While we know demand for housing is strong, but if we are to keep things in balance we need to see increased supply. Supply is only going to come from one of two places - existing homeowners listing their homes for sale or new construction.

While home builders have been building as fast as they can there is a long lead time. New home builder confidence is at an all-time high and a record number of housing permits are being issued which tells me more supply is coming.

To make up the difference in the meantime we need to see more existing homeowners list their homes for sale. This hasn’t happened for a couple of reasons;

1) Why would someone list their home for sale when they have nowhere to go? One fear current homeowners have is selling their current home with the uncertainty of being able to find a replacement home and ending up “homeless”. I talk about options to that problem in last weeks blog post.

2) It has been suspected that many would-be home sellers from 2020 decided not to put their homes on the market due to uncertainty. A recent survey of these potential home sellers confirmed this suspicion.

The belief is that many of these sellers will return to the market later this year as the direction on where things are heading, in terms of the pandemic and the economy, becomes more clear.

Distressed Properties

One fear, as unemployment skyrocketed as a result of the pandemic, was that housing was going to face another foreclosure crisis. The fundamentals of the housing market in 2020 were very different from what was being experienced in 2007, 2008, and 2009.

In total, about 5.4 million households entered into mortgage forbearance programs and approximately 2.7 million households remain in one.

As you can see from the chart above, 51.7% of those that entered mortgage forbearance have since left the program. Of those, 28.6% never actually needed it and continued to make their mortgage payments, some loans have been paid off in full, most likely through a sale, and 15.6% have since brought their loans current.

Of those households still in the program, 33% have either received a loan modification or a loan deferral (payments missed were added to the back of the loan.)

15.3%, or approximately 413,000 households, remain in the program and could possibly end up in the foreclosure process.

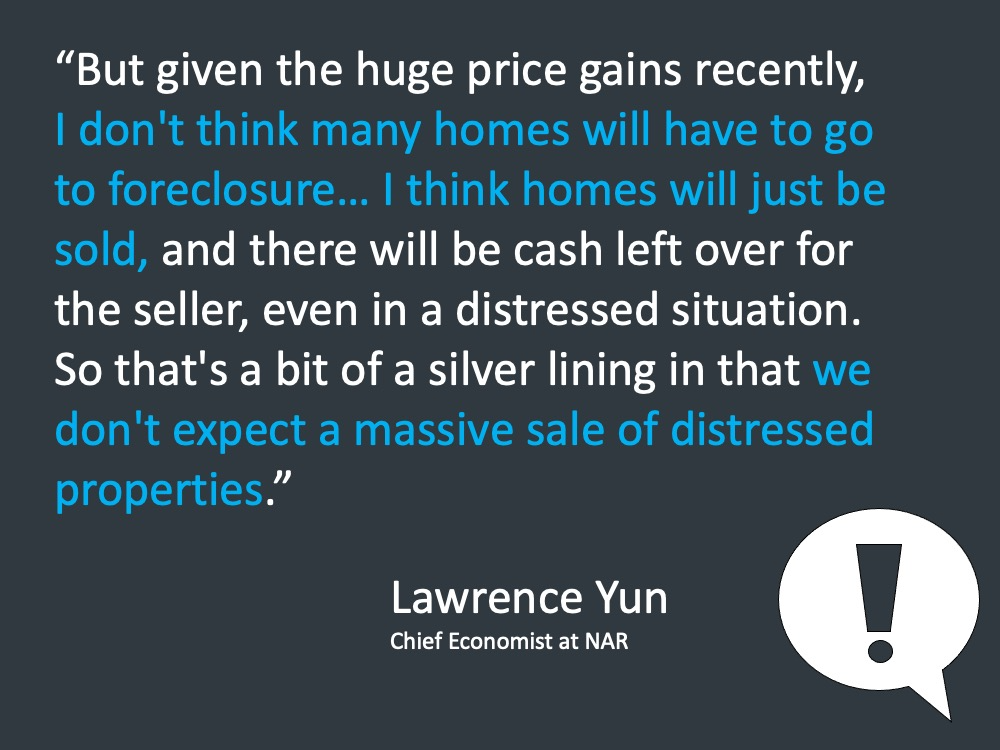

Home price appreciation over the past decade has provided options that didn’t exist during the previous housing crisis. It is currently estimated that only 3% of all mortgaged households in the country are currently in an “underwater” position. That means if someone in trouble does need to sell there is a high likelihood they could sell, pay off their existing mortgage, and have money left over to move. I’m certainly not trying to downplay, or make light of the situation, but am pointing out that the number of homeowners in trouble does not amount to a foreclosure crisis that would have a significant impact on the real estate market of today. If all of the homes in trouble ended up being listed for sale they could easily be absorbed by current demand.

If you have been thinking of buying, or considering selling this year, and need help understanding all of your options, CLICK HERE to schedule a free consultation. Let’s work together to develop the plan thats right for you.