The current real estate market is crazy, to say the least. Homes are receiving multiple offers within just a few days of being listed, bidding wars are the norm, buyers are getting frustrated, and sellers seem to still be in hibernation! While every market has its challenges, this is one of the most challenging markets I have experienced in the nearly 20 years that I have been in the business.

In this month’s real estate market update, I take a step back in an effort to explain how we got here. This market isn’t the result of any one factor, but several different factors, some of which have been years in the making. Watch the following video, or continue reading below, to learn more about how we got here and how long the current market conditions are likely to last.

Searching for a Home in Frisco or Prosper? CLICK HERE to see the Newest Listings

The Impact of Supply and Demand

If you have seen any of my recent blog posts or videos, then I’m sure you’re familiar with supply and demand as it relates to real estate and home prices. Demand has been increasing for several years now and surged following the initial lockdowns of the pandemic a year ago. Much of this rising demand has come from Millennials, the largest generation in the US as of 2019, who are reaching their prime home-buying years.

At the beginning of the pandemic it was widely predicted that Covid would have a negative impact on the real estate market as overall demand for housing, especially in light of economic uncertainty, was expected to decline. The opposite happened! I think it’s safe to say the definition of “home” has changed in the last year. Rather than being the place you are when not at work, school, or on vacation, home became where you work, go to school, and spend a vacation. This phenomenon caused people to reassess their housing needs with many deciding their current “home” no longer fit their needs as well as it used to.

The economic stimulus as a result of the pandemic impacted mortgage rates in a positive way for homebuyers by pushing rates to historical lows. These record-low rates only added fuel to already increasing housing demand. Here’s a look at how mortgage rates dropped as a result of the pandemic:

After falling for much of 2020, mortgage rates started to rise in early January and have risen more sharply in the past 3 weeks (see last week’s blog post The Impact of Rising Mortgage Rates on Home Buyers and Sellers.) These rising mortgage rates have already started to soften demand as new mortgage applications have dropped and are now about even with year-ago levels. Although rates are expected to continue rising, especially as the economy continues to improve, most experts do not predict that rates will go above 3.2% or 3.3% this year.

How About Supply?

Rising demand wouldn’t be enough to cause current real estate market conditions if it wasn’t coupled with dwindling supply. Current market conditions are a result of the fact that we have had rapidly rising demand AND falling supply. The supply side of the equation is a problem that has been brewing for over a decade now and can be traced back to the market crash in 2007, 2008. When the real estate market collapsed in the mid to late 2000s, new home builders got stuck with a lot of inventory they couldn’t sell and took a beating financially. As a result, new home building slowed substantially. When the real estate market recovered home builders took a steady as she goes approach. Think of new home building like trying to make a u-turn on a cruise ship. It doesn’t happen immediately. As the market recovered it took the builders quite a while to ramp construction back up again. As a result, the supply of homes being built wasn’t enough to keep pace with the number of new households being created due to population growth. How big of a deficit was created? A big one, as shown on the following graph:

As you can see, 2020 marked the 13th straight year that we failed to build enough homes to match the average number of single-family homes built annually (just over 1 million) between 1970 and 2006. Currently, 2021 is the first year we are expected to reach the 50 year average number, but when you consider how under built we have been for the past 13 years, especially when compared to 2000 through 2006, you can begin to see how big of a problem supply currently is.

There are two places that housing inventory comes from, new construction and existing homes being resold. We know how far behind we are in new construction homes and as Odeta Kushi mentioned above, existing homes coming on the market has lagged what we normally see. As the vaccine continues to get rolled out and the economy continues to improve, it is expected that more resale homes will come on the market. While any increase in inventory will help, it will take some for conditions to improve substantially.

In Frisco, new listings for February were down 40.3% year over year and the total number of homes for sale is down 76.8% compared to this time last year.

In Prosper, new listings for February are down 54.8% year over year and the total number of homes for sale is down 85.1% compared to last year.

The result of this decline in homes for sale means we currently have about a 2 week supply of inventory. Keep in mind, 6 months’ worth of supply is considered normal for a balanced market. As a reminder, supply in real estate refers to the length of time it would take all homes currently listed for sale to sell at the current pace of sales. Saying conditions strongly favor sellers at the moment would be an understatement.

You can clearly see how the number of homes for sale has changed over the past 3 years on the following graph. The blue line represents Frisco and the red line Prosper.

In Temecula, CA my team is experiencing similar conditions. New listings are down 24.8% year over year and the total number of homes for sale is down 49.4% compared to last year. As a result, inventory is down 55% to just under a 1 month supply.

The Impact on Home Prices

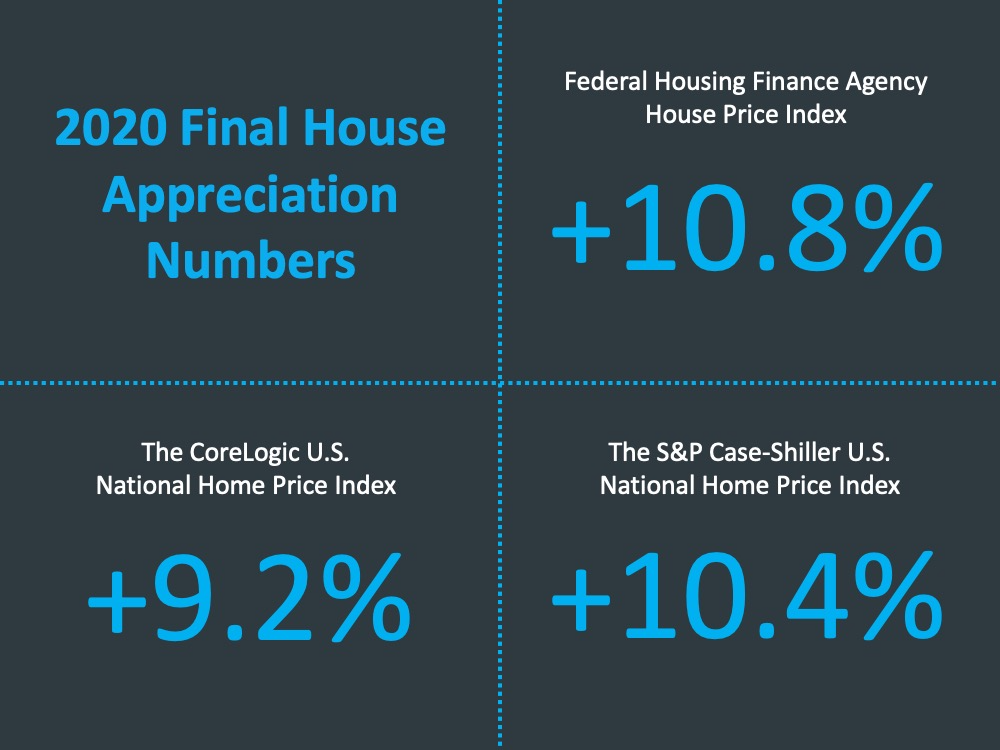

Since home prices are directly related to supply vs demand it should come as no surprise that home prices continue to rise. The final numbers for 2020 have just been released:

Although slightly different depending on the data source, nationally, home prices rose about 10% last year. The pace of appreciation in all of the markets we work in was higher than the national average.

Year over year median price increases for both Frisco, TX and Prosper, TX was 15%

Year over year median price increase for Temecula, CA was 19%

The change in median prices over the past 3 years can clearly be seen on the following graphs:

Although there will always be up and down movement from month to month depending on the number and type of homes sold, the trend is clearly visible and the pace of appreciation the past few months, as inventory has shrunk dramatically, has certainly accelerated.

Where Do We Go From Here?

As mentioned above, the number of resale homes that come on the market is expected to increase as we move further into this year. There may not be a dramatic increase in resale inventory in the next couple of months, but we should start to see more homes come on the market. Additionally, new home builders continue to bring new communities online and release additional phases. Any increase in inventory, coupled with a softening of demand due to rising interest rates, will bring some relief to the market even though we might not immediately notice it.

The imbalance between supply and demand will also cause home prices to continue to rise this year. The forecast on how much prices are expected to increase has recently been revised upwards, but appreciation is expected to be lower than last year.

Bottom Line

As prices continue to increase questions on home affordability will continue to be raised. How much affordability is impacted depends on how much mortgage rates end up rising this year. Low mortgage rates, coupled with rising wages, have kept affordability in check so far, but that will vary from market to market.

For Buyers

The market is frustrating without a doubt. Only you can decide what is best for you and your family. If you decide to take a break and wait in hopes of things settling down know that there is an opportunity cost in waiting. A 1% increase in interest rates lowers your purchasing power by approximately 10%. Meaning, if you were pre-approved for $500,000 at 2.5% and mortgage rates go to 3.5%, the amount you are pre-approved for will drop to $450,000. In an environment of rising home prices that can make a big difference to the type of home you are qualified to buy.

For Sellers

If your goal is to sell for the highest possible price in the shortest amount of time then market conditions are currently in your favor, but with prices still rising should you sell? That depends, If you plan on selling and moving to a larger, more expensive home, then your next home is getting more expensive as well, especially as mortgage rates rise. If you plan on selling and downsizing to a smaller, less expensive home, now might not be the best time for you to make a move as there is a good chance your current home is going up in value more than your next one is.

Truthfully, trying to time the real estate market is like trying to time the stock market. The best time to make a move is when it’s the best time for you to make a move when all circumstances are taken into consideration, not just price.

If you'd like to talk through your real estate goals in more detail please feel free to Schedule A Call with me. There is never a cost or any obligation.