Should you expect a big drop in home prices in 2023?

Are the first signs of a housing market crash many buyers are hoping for starting to appear?

The experts have just released their latest forecast for home prices in 2023 and they don’t all agree on where home prices are heading. What they do agree on is where you live will greatly impact how the housing market performs and we are not heading for another 2008-type market crash.

Watch the following video, or continue reading below to see the latest forecasts and learn how you can stay up to date on the latest trends in the city/zip code of most interest to you.

Will Home Prices Fall in 2023

Home prices have been the main topic of conversation for many of the potential buyers I have spoken to over the past few weeks.

Most have said a version of the exact same thing, "we're still really interested and want to buy, but are going to wait for prices to come down.”

So the question is, are they going to come down? If so, by how much?

If that sounds familiar, or if you can relate to that sentiment, I want to start off by saying the honest truth is nobody knows for sure exactly what's going to happen with home prices. If you go back and look at everything that's been published over the last couple of years, you'll see that opinions vary, and forecasts change.

Nobody has a crystal ball.

Nobody knows exactly what’s going to happen going forward.

With that in mind, my goal here today is not to convince you that now is, or isn’t, a good time to buy or sell a home. I'm simply trying to share the latest information and data that enables you to make the best decision for you based on the facts and not a headline that does little more than promote fear.

So with that in mind, let's jump into it.

As I mentioned above, many potential buyers I have spoken to are sitting on the sidelines waiting for home prices to fall. Here's what Taylor Marr, Deputy Chief Economist for Redfin recently had to say about that;

What Taylor is referring to is the expectation from earlier this year that rising mortgage rates would cut the legs out from under buyers causing demand to fall through the floor. The lack of demand would put downward pressure on home prices as supply rose.

What wasn’t expected was the fall in supply coming to market. As such, we haven’t really experienced the large imbalance between supply and demand needed to force home prices down significantly. Here in Frisco and Prosper, home prices have fallen from their highs in April and May respectively, but the median sales price actually ticked back up in September.

Why did supply fall?

Let's face it, if you own a home right now and were thinking of selling but you didn't necessarily have to, why would you? You're probably locked in with a mortgage rate around 3%, and, depending on how long you’ve owned your home, are sitting on a substantial amount of equity. So why sell? If you put your home on the market and weren’t able to get the price you wanted, you’d dimply take it off the market, and that’s exactly what we’ve been seeing.

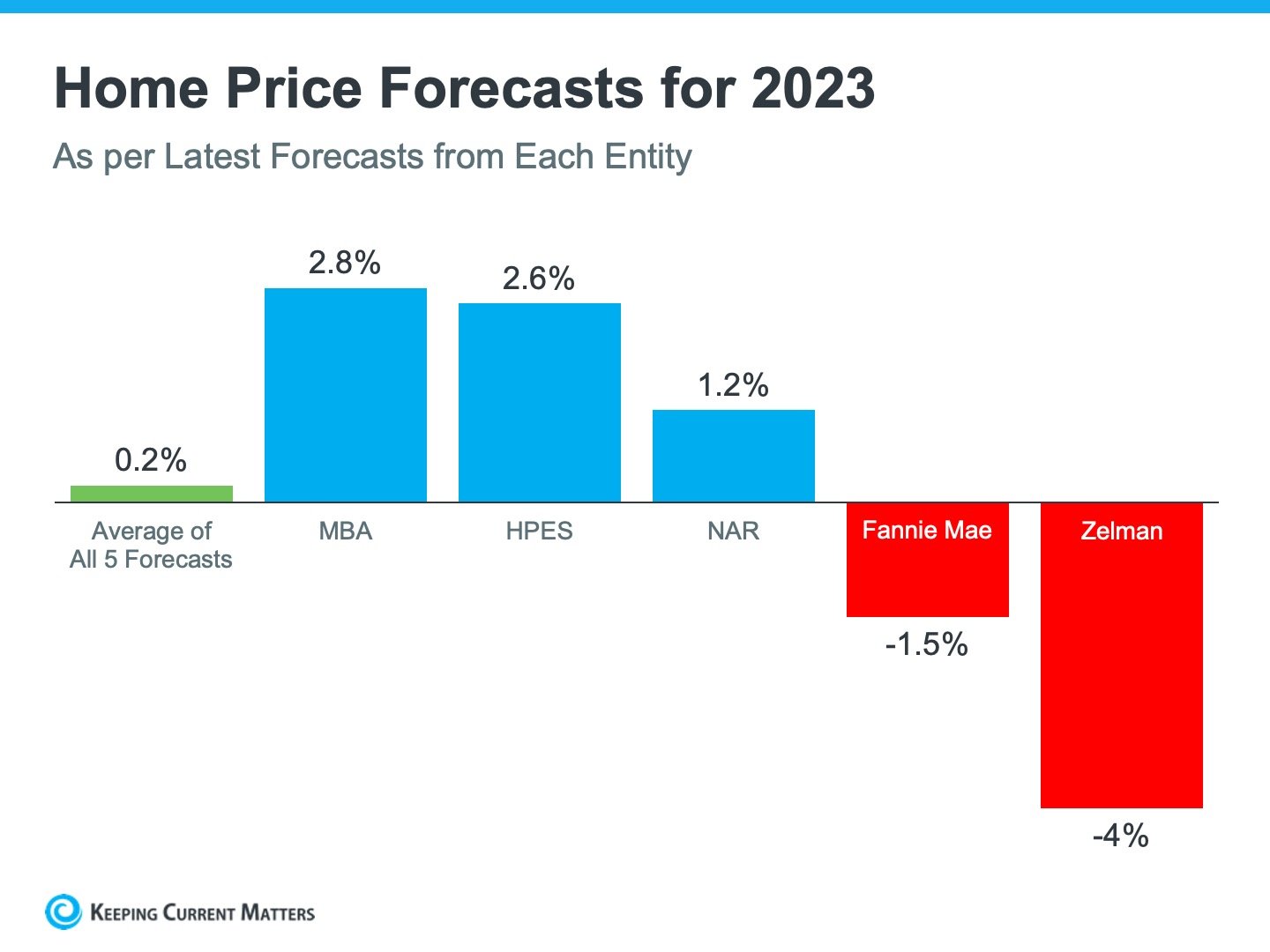

The data is showing us that once mortgage rates rose above 5.5%, buyer demand slowed drastically. That, coupled with general economic uncertainty, has resulted in downward adjustments to home price expectations in 2023;

While home price appreciation forecasts were lowered by all of the entities, Fannie Mae, which had been forecasting prices to increase in 2023, have now flipped into the red column to join Zelman & Associates.

These aren't drastic drops and certainly not the drops that many home buyers had been expecting or maybe even hoping for that would result from crash type conditions, but they do represent very different conditions than we have been experiencing the past couple of years.

Could this change tomorrow?

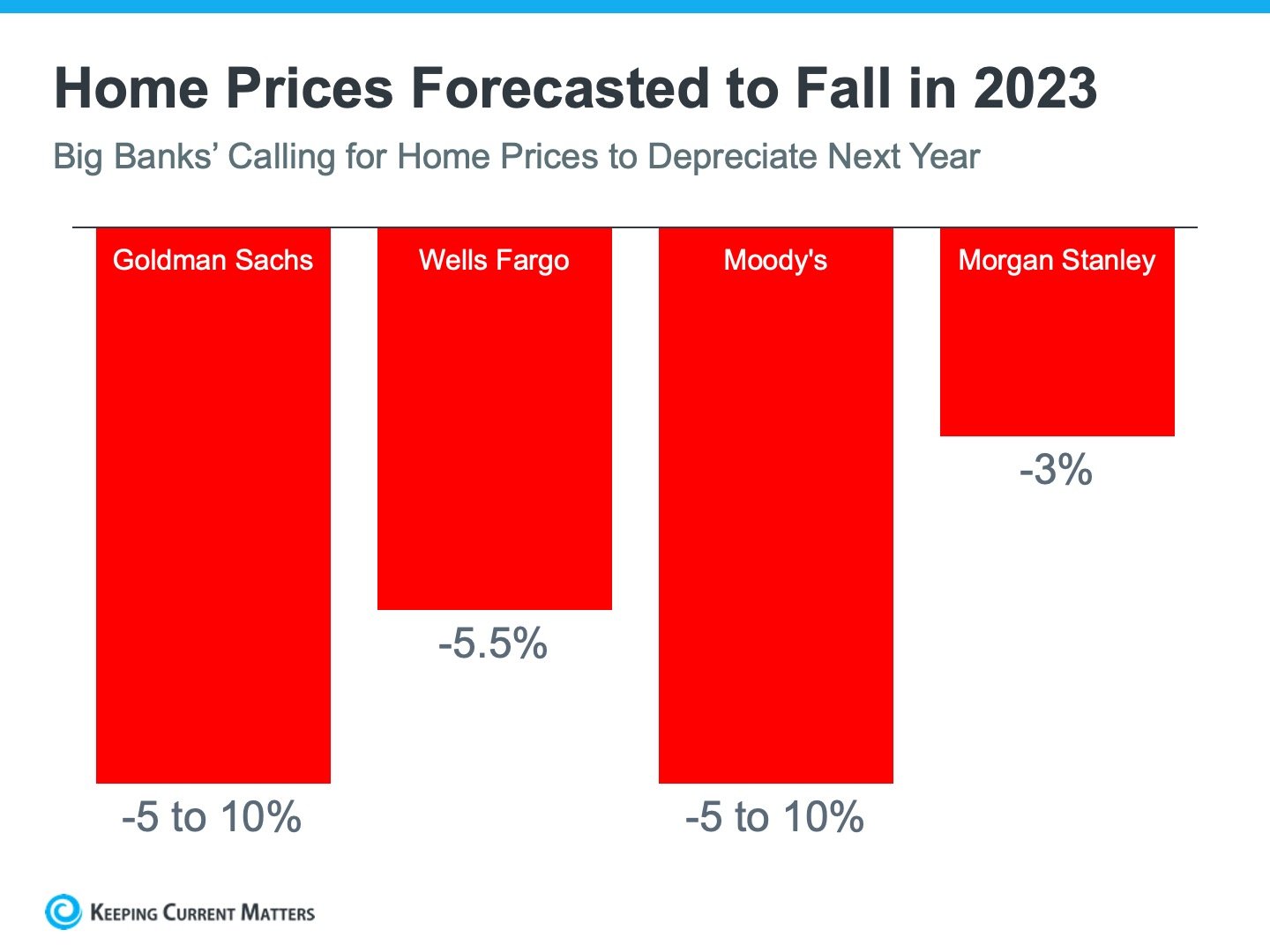

Absolutely. As a matter of fact, not all institutions are in agreement. Notably, the major banks are all expecting the housing market to experience a sharper downturn in 2023 as shown in this forecast;

Goldman Sachs are forecasting home prices to fall between 5% and 10% in 2023, Wells Fargo is forecasting home price declines of 5.5%, Moody's, like Goldman-Sachs, a drop between 5% and 10% and Morgan Stanley, a drop of up to 3%.

As mentioned previously, these forecasts are looking at a national average, but every single market is unique and every market will respond differently.

Moody's explained that the 5% to 10% they are forecasting could be experienced in the most vulnerable markets, Boise, Phoenix, Austin and other areas that saw the most rapid price appreciation over the last 2.5 years. Those are the markets that will have the most exposure for downward pricing pressure.

Even though these forecasts are calling for steeper declines than the first forecast, it's important to point out they aren't catastrophic drops. (Check out my recent video - Is This a Housing Market Crash or Correction)

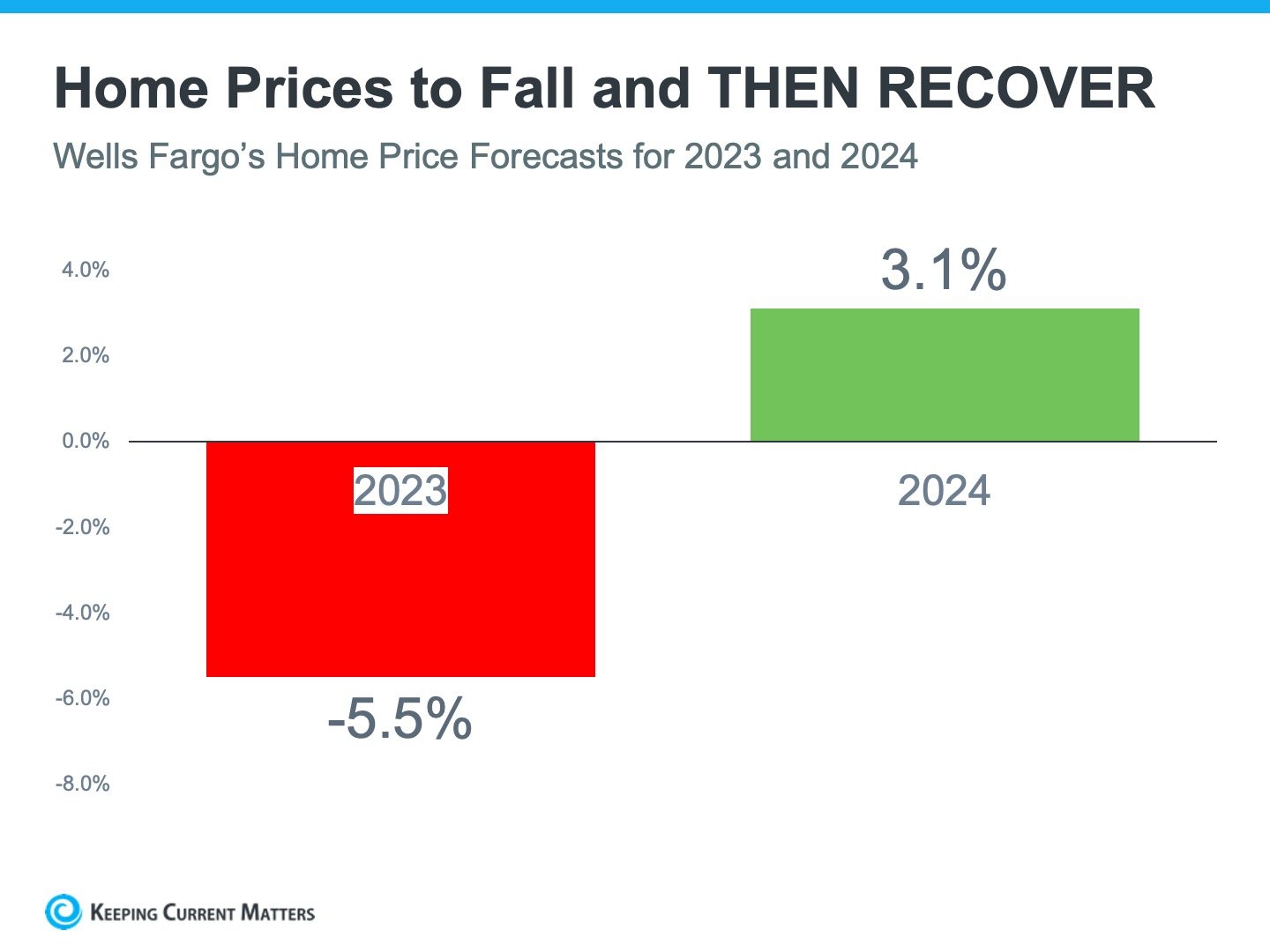

What About 2024

While any reduction in home prices would bring relief to weary buyers, even the big banks don’t expect a prolonged downturn and expect prices to recover as soon as 2024 as shown in this forecast from Wells Fargo;

As mentioned, every market will respond differently. Here in Frisco and Prosper, TX the median sales price is already down approximately 14% from its peak earlier this year, but home prices are still 14% higher than a year ago in Prosper and 20% in Frisco.

The majority of forecasts I’ve seen for our local markets in 2023 continue to show price appreciation but at a much more moderate pace of between 3% and 5%.

Want to stay up to date on your local housing market? CLICK HERE to view my Frisco Market Report and from that report search and city/zip code in the country and subscribe to receive weekly updates.

Mortgage Rates

While all of the focus of this blog, and the majority of conversations I’ve had with potential buyers, have centered around home prices, mortgage rates are more important when it comes to affordability,

Let me explain…..

There is a reason the vast majority of new homebuilders, in their current incentives, are offering mortgage rate buydowns rather than just price reductions.

The median sales price of a home in Frisco last month was nearly $650,000.

If we assume a standard conventional loan with a 10% down payment and a 7% mortgage rate, the monthly principle and interest mortgage payment would be $3,892.

Using the worst-case scenario forecast of a 10% drop in home prices, the price of the $650,000 home in our example would come down to $585,000. Using the same mortgage type and terms, the monthly P&I payment would now be $3,502, a savings of almost $400 per month.

On the other hand, if, instead of a reduced price, you were to purchase the home in our example for $650,000, the same type of loan, but obtain a mortgage rate of 5%, the monthly P&I payment would be $3,140, a savings of $751 per month.

How do you obtain a 5% mortgage rate when rates are 7%? With a buydown program.

If you’d like to know how to incorporate a buydown program in your home purchase plans, Schedule a Call with me and I’d be happy to discuss this with you.