What a difference a month makes!

After talking about signs of a change in the real estate market for the past several months, that change is most definitely here as you’ve probably noticed.

Before thinking the real estate market is about to go into a freefall, understand the market is still hot but not white-hot like it has been the past couple of years.

Mortgage rates, the question of a correction, and ever-increasing talk of a recession have been the main storylines and are the focus of this month’s real estate market update.

Watch the following video, or continue reading below, to learn more;

Mortgage Rates

Mortgage rates, which started the year in the low 3% range, jumped 2% to 5.1% by the third week of April. Since then, mortgage rates had been relatively stable through the first week of this month.

In an effort to combat inflation, the Fed announced earlier this year they would begin raising the benchmark rate by 0.25% to 0.50% at each of their policy meetings. That announcement is partly what triggered the increase in mortgage rates we saw earlier in the year. Rates had been holding stable because the future anticipated actions of the Fed had already been priced into current mortgage rates.

Following the latest inflation numbers released last week, which were higher than expected, the Fed announced yesterday they were seriously considering raising interest rates at the June meeting by 0.75% instead of 0.5%.

The stock market reacted negatively to the news, as did mortgage rates, which jumped to just over 6% before settling back into the 5’s this morning.

While the Federal Funds Rate doesn’t directly impact mortgage rates, which are more closely tied to the 10-year Treasury Bond yield, continued uncertainty about the economy is likely to cause rate volatility over the coming months and is fueling talk of a recession, which I’ll discuss further later.

Rising mortgage rates coupled with rising prices across the board are starting to impact buyer demand. As a result, we are starting to see a return of adjustable-rate mortgage products.

No, these are not the loans that were widely used in the early 2000s that led to the housing market crash as these loans still require good credit and full documentation to qualify, but they offer lower interest rates for the first 5 to 7 years of the loan, which can be a solid option for many first time buyers who are more likely to move again sooner than later.

Are We Heading for a Correction?

None of the experts think so based upon the true definition of a correction;

Semantics aside, the honest answer to the question of a correction will really depend on where you live.

Overall, the average of all expert opinions is for home prices to climb 8.9% in 2022, which is certainly lower than the 20+% we have seen in the past couple of years.

Here in Frisco, TX, Zillow is forecasting 13.5% home price appreciation over the next 12 months.

It’s important to remember the rapid home price appreciation we have experienced has been due to very high demand against record low supply. Although demand has softened in the face of higher mortgage rates and high inflation, it hasn’t disappeared. Locally, we are still seeing multiple offers and bidding wars, but not as many.

A new home community I visited over the weekend let me know a home that had recently been released received 6 offers compared to over 30 on a home released just a month ago.

Inventory (supply) continues to rise and is currently 13% higher than a year ago, but the 396,000 homes for sale nationally is still well below the 950,000 homes for sale nationally in June 2019.

While the news continues to be full of reports of declining mortgage applications and declining home sales, it’s important to keep things in perspective and remember that these are declines from record-high levels.

Take a look at this graph from ShowingTime, which tracks home showing activity;

While showing activity is at its lowest level since December, and certainly fell again in May, it is still substantially higher than pre-pandemic levels.

Although the real estate market is expected to continue slowing (normalizing) over the coming months, none of the leading experts believe we are going to experience a dramatic downturn.

Moody’s Financial is known for issuing some of the most conservative outlooks on housing. Mark Zandi, Moody’s Chief Economist, believes some of the most overvalued markets could experience price declines of between 5% and 10%, but expects the majority of the country will see prices remain flat over the next year or two.

What About a Recession

As inflation remains high there is a growing belief among Fortune 500 CEO’s that the Fed will not be able to tame inflation without sending the economy into a recession. Some even believe we might already be in one.

While the last major recession could more accurately be described as a depression, it’s important to remember they don’t always mean doom and gloom and are a natural part of the economic cycle.

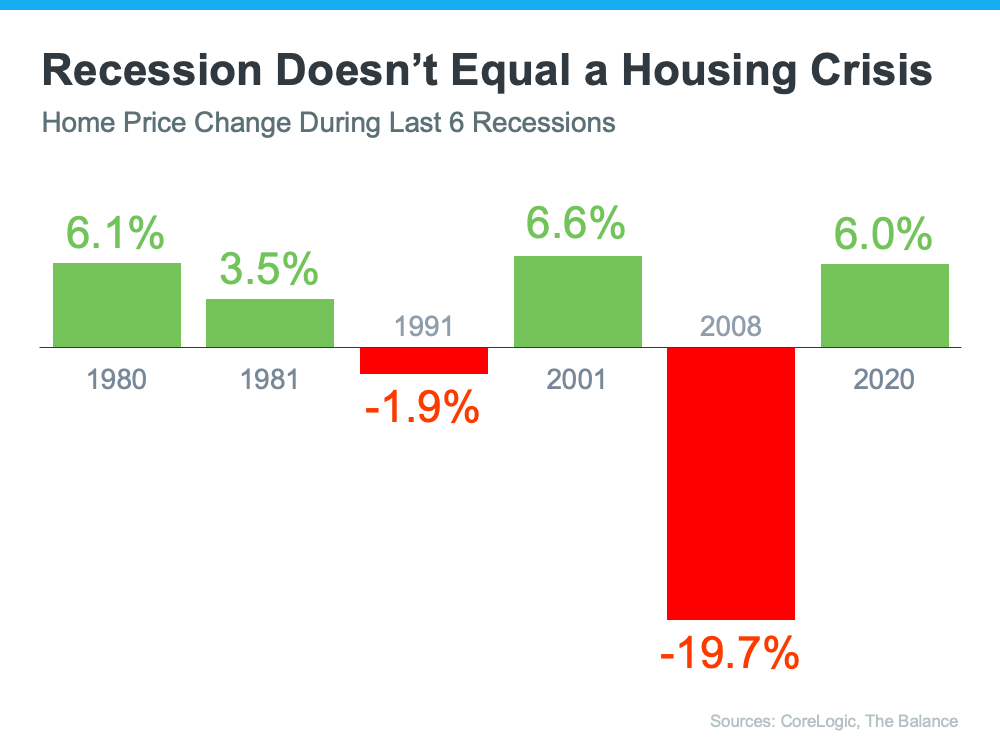

With regards to housing, home prices have actually increased in four of the past 6 recessions as shown on the following graph;

The big exception was 2008 and I haven’t found one expert forecasting anything like that over the next few years.

While nobody knows for sure what the future holds, all indications are that the real estate market will continue to move towards a more balanced market, which is good news.

Click Here for the Latest Frisco Market Trends

Bottom Line

While home prices are expected to keep rising locally, they should be at a much slower pace than we have seen over the past couple of years.

Home buyers should expect more choices, fewer bidding wars and multiple offer situations, while sellers will need to pay more attention to initial pricing and expect days on market to increase.

Is now the right time for you to consider buying or selling a home?

Give us a call at 469-296-5230 or email Contact@S2RealEstateTeam.com and let’s discuss it.