We can all agree that homes are less affordable now than they were at this time last year.

Rapidly rising prices coupled with higher mortgage rates have forced many potential buyers to the sidelines in the hope that a market crash will be the reversal of fortune they are looking for.

But what if the market doesn’t crash?

For the record, I don’t think the market is going to crash, as explained in last week’s blog post, but do expect the market to cool and find balance, especially here in Frisco and Prosper.

With that in mind, in this blog, I’m going to give you 3 options to consider if you are in the market to buy a home.

Continue reading below, or watch the following video, to learn more;

It’s not always feast or famine!

There seems to be a common belief going around that a rapidly appreciating housing market must always be followed by a crash. That belief is simply not true.

We can see a softening, or even experience a correction, without it being a crash.

The housing market crash we experienced in 2008 was a result of the house of cards that had been built in the years prior. Basic market fundamentals no longer applied and demand was being fueled by countless exotic loan problems that had no option but to end badly.

Today, the fundamentals of the housing market remain strong and the changes in pricing we have seen have been a result of the imbalance between supply and demand.

Low supply, due to a decade of being underbuilt, was exaggerated by pandemic-driven supply chain issues impacting everything from brick to windows, appliances, and ducting.

Already strong demand, due to new household creation and the millennial generation reaching prime home-buying age, was exaggerated by a monetary policy that created historically low, and unsustainable, fixed-rate mortgages.

The perfect storm!

What we are experiencing now is the calm after the storm and how this plays out over the next couple of years will largely depend on where you live.

Here in north Texas, we have a very strong economy, continued job growth, very low unemployment, and inbound migration meaning our housing market will react differently than cities and states not experiencing the same thing.

That being said, rising home prices and mortgage rates have made buying a home more expensive and caused housing affordability to drop to the lowest level in over 30 years.

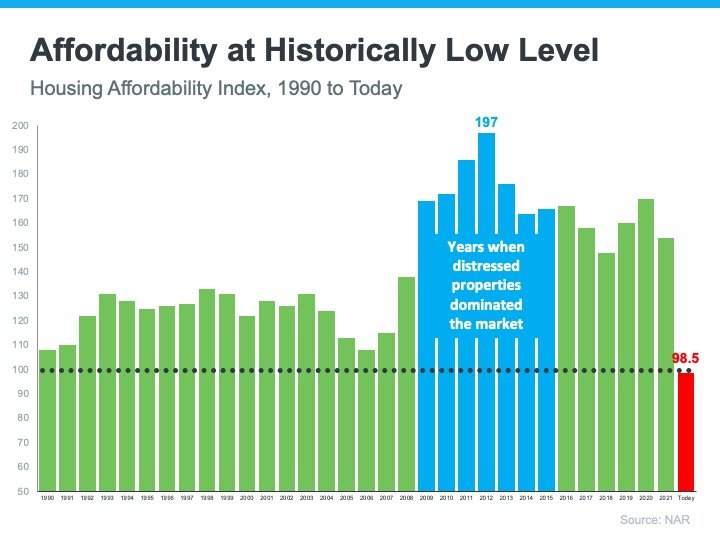

Housing Affordability

Housing affordability is calculated based on home prices, interest rates, and wages.

Here is a graph showing national housing affordability going back to 1990;

The black dotted line represents the level at which the average wage earner can afford the average-priced home.

While the current reading of 98.5 is not far below the line, it does represent the first time we have fallen below that line since 1990.

The rise in home prices alone did not cause home affordability to drop below the line. Mortgage rates jumping from 3% to 5.75% was the missing ingredient. On average, mortgage payments are 53.7% higher today than they were a year ago. While wages have also grown, they have grown enough to offset rising home prices and mortgage rates.

Debt to Income Ratio

When a potential home buyer applies for a loan, one of the items the lender considers is the debt-to-income ratio.

Generally, a lender does not like to see the monthly principal and interest payment be more than 25% of the total monthly income.

Here are the average debt-to-income ratios for mortgage borrowers since 2000;

While having a debt-to-income ratio over 25% does not automatically mean you won’t qualify for a mortgage, especially if you have no other debt, it does mean that affordability is trending in the wrong direction.

3 Options for Potential Home Buyers

As mentioned above, home affordability is comprised of home prices, interest rates, and wages. While home prices have come off their peak from a few months ago, it currently doesn’t look like home price declines will be enough to solve the affordability question for many buyers.

Mark Zandy, Chief Economist for Moody’s, believes we will see a correction, but not a crash, and estimates prices will decline between 5% and 20% from their peak depending upon where in the country you live. Considering home prices here in Frisco and Prosper have increased by more than 20% in each of the past 2 years, even a 20% drop in prices means homes will still be more expensive than they were a year ago.

For the record, I’m not expecting we will see a drop anywhere near that based on the strength of our economy here locally.

The latest forecast of mortgage rates indicates we should expect to see mortgage rates between 5% and 6% for the next year before settling around 4.5% by the end of 2023 barring anything unforeseen happening.

With that in mind, here are the 3 options to consider;

Expand your search area - while focusing your home search on Frisco and Prosper might be what you want to do, expanding your search to Little Elm, Celina, Aubrey, Anna, and Melissa might offer you additional options. You can currently find new homes in Celina, within Prosper ISD, for under $400,000. Buying further out than you want might not be ideal, it’s exactly what my wife and I did when we bought our first home. Not being able to afford to buy in the area we had been renting, we looked further out and were able to find a larger home, on a larger lot, for substantially less money.

Explore all financing options - there’s a saying going around right now “marry the house, date the rate.” As mentioned above, mortgage rates are expected to decline in the coming years. With that in mind, if you find a home you love you might want to consider an adjustable-rate mortgage that will lock in a lower rate for the first few years. You will be able to refinance at a later date when mortgage rates come back down. Talk to your lender to explore all financing options available to see what makes the most sense for you. If you’d like us to refer you to our preferred lending partner please reach out and we’d be happy to do that. Alternatively, many new home builders are currently offering incentives to “buy-down” the interest rate so you are apply to purchase today and still receive a fixed rate mortgage around 4%. Reach out to us for additional information on builder incentives.

Explore grants and special programs - in addition to the information your lender can provide, there are often different grants and down payment assistance programs available that many potential buyers don’t know exist. A great website is downpaymentresource.com where you can explore grant and assistance programs by county.

Bottom Line

Everyone’s situation is different. For some, continuing to rent, especially if you are locked in at a good rent, might be the best option. For others, exploring all options to buy a house and get into the market could be the best way to go.

If you’d like help to explore all options available for you and your family please reach out as we’d be happy to talk with you. You can call us at 469-296-5230 or email Contact@S2RealEstateTeam.com