Mortgage Rates Update: Why Are Mortgage Rates Rising After the Federal Reserve Cuts Rates?

If you've been keeping an eye on mortgage rates, you may have noticed something curious. Despite the Federal Reserve cutting interest rates by half a percent, mortgage rates actually went up! How is that possible?

In this post, we’ll dive into why this happens, what to expect from mortgage rates in the coming months, and how it could impact home prices in Frisco, TX.

The Federal Reserve and Mortgage Rates – What’s the Connection?

It’s important to understand that the Federal Reserve doesn’t directly control mortgage rates. When the Fed lowers its federal funds rate, it affects loans like credit cards and home equity lines of credit. Mortgage rates, however, are tied to the 10-year Treasury bond.

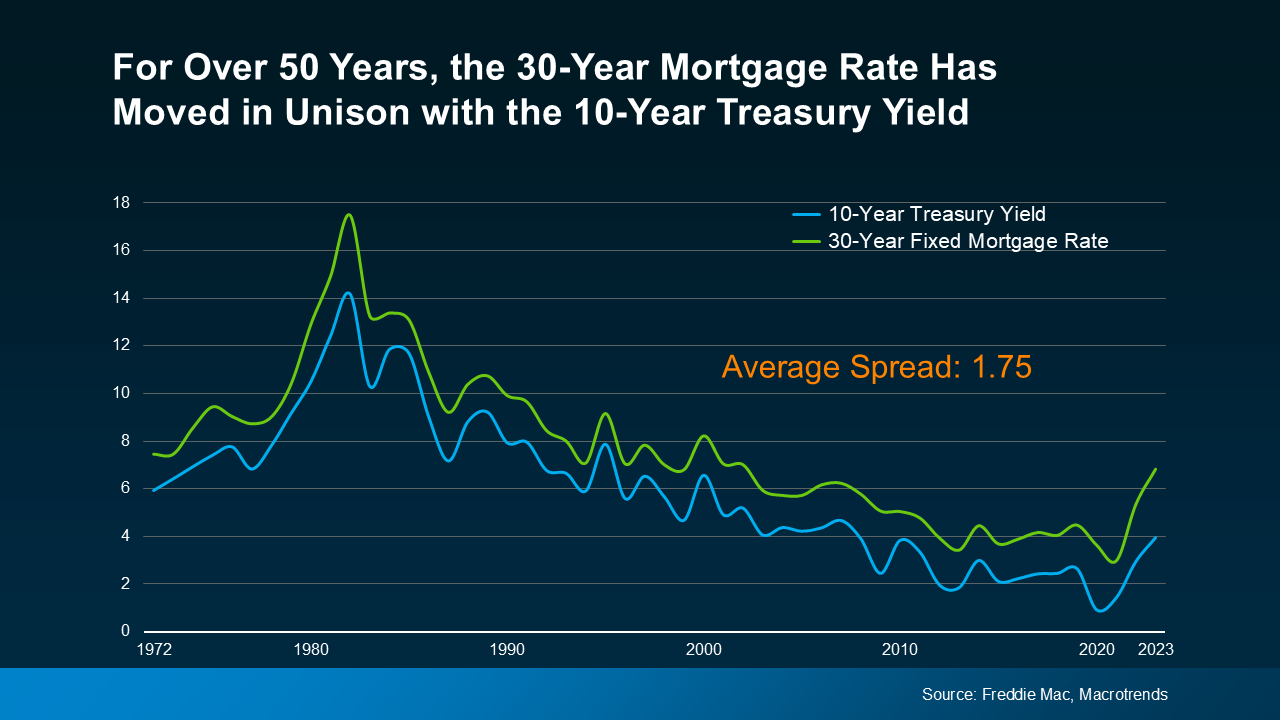

The relationship between the 10-year Treasury bond and mortgage rates is pretty straightforward: when the Treasury yield moves, so do mortgage rates. But the gap, known as the "spread," is what adds complexity. Historically, the spread between the 10-year Treasury bond and mortgage rates has been about 1.75%. Currently, that spread is higher than normal, at around 2.375%, indicating continued uncertainty in the market.

Here’s a visual of how these two rates mirror each other over time. The more uncertainty in the market, the greater the spread between them, and this helps explain why mortgage rates have been slower to fall.

For a more detailed explanation on why the spread is higher than average, check out the following video:

Where Are Mortgage Rates Headed?

Looking ahead, experts expect mortgage rates to continue their downward trend. If the spread between the Treasury yield and mortgage rates narrows back to its historical norm, we could see mortgage rates between 5.2% and 5.6%. This would be a welcome relief for homebuyers, especially compared to the rates we've seen hovering in the mid to upper sixes over the past year.

Impact on Home Prices

Now, what does this mean for home prices? In Frisco, TX, home prices have remained stable, largely thanks to the area’s robust supply of new construction homes. Buyers here benefit from the steady inventory of new homes, but with many homeowners locked into low mortgage rates from previous years, the resale market has been slower.

As mortgage rates continue to drop, we expect to see more buyers come back into the market, which could increase competition and potentially drive prices higher. Without a significant change in supply and demand, there’s nothing in the data to suggest that home prices will decline.

Should You Wait or Buy Now?

One of the biggest questions buyers are asking is, “Should I wait for mortgage rates to fall further?” While waiting might give you more options in terms of inventory, it also means competing with more buyers during the peak season. Plus, with rates already on a downward trend, waiting could mean missing out on a great deal now.

If you’re on the fence, Schedule a Free Consultation and let’s discuss your unique situation in more detail. I’d welcome the opportunity to share additional information so you can make the decision that’s best for you and your family.

In Conclusion

Navigating the housing market is all about timing. With mortgage rates fluctuating, it can feel like a bumpy ride, but staying informed is key to making the right decision. If you’d like to stay updated with weekly market reports, Click Here for the Frisco Market Report or use the search feature at the top of the report to see the latest trends for the city or zip code of interest to you.