Considering home prices are continuing to rise, mortgage rates have jumped significantly, and inflation is at a 40-year high, is now still a good time to buy a home, or should you put those plans on hold until 2023?

While I certainly don’t pretend to have all the answers, my goal in this blog post is to share the latest information, along with a few insights, to help you make the best decision for you and your family.

Watch the following video, or continue reading below, to learn more;

Uncertainty Abounds

In talking to people over the past couple of weeks, what has become clear is that there is a general sense of uncertainty right now. While the fundamentals of the housing market remain strong, and no leading indicators suggest a problem in the months ahead, the fact that mortgage rates have jumped and everything from gas to food has become so much more expensive, it just feels like something is about to change.

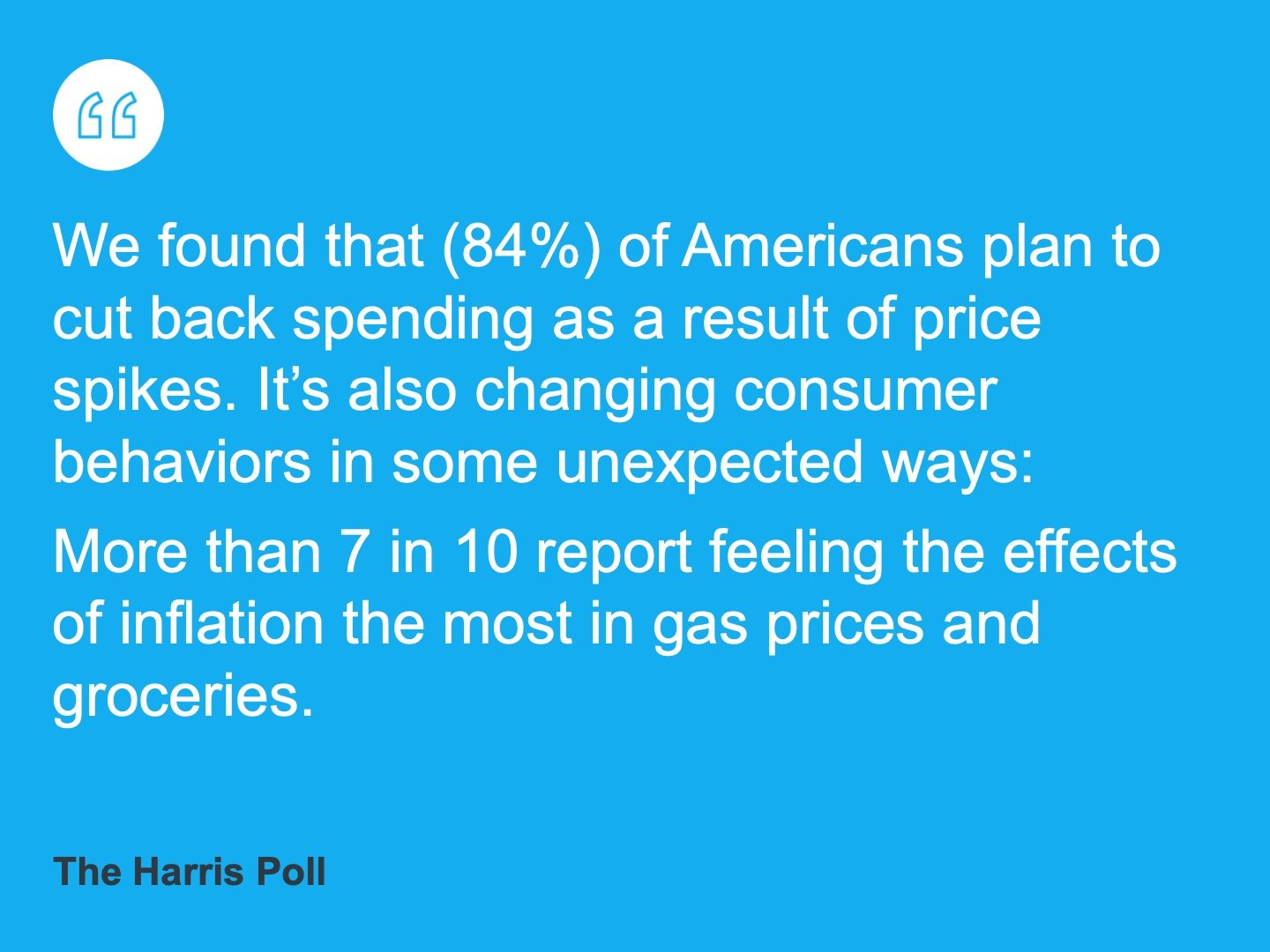

I’m not alone on this either, as the results of a recent Harris Poll show that rising prices and economic uncertainty are causing the majority of Americans to change some of their spending habits;

As discussed in last week’s blog, the massive imbalance between supply and demand over the past couple of years has been the root cause of rising home prices.

Record-low mortgage rates helped to offset those home price gains, but with rapidly rising mortgage rates and high inflation, affordability is becoming a bigger issue that will impact the housing market in the months ahead.

While we did see an increase in real estate activity the past couple of weeks, that increase was a result of homebuyers jumping into the market in an effort to secure a home before rates and prices rise further.

Buy Now or Wait

That is a decision that only you can make and will be different for everyone, but there is a cost to waiting.

One thing to keep in mind is that a 1% rise in mortgage rates lowers the price of the home you can afford to buy by approximately 10%. If you were pre-approved for a $500,000 purchase price at 3.5%, at 4.5% your pre-approval will now only be for $450,000.

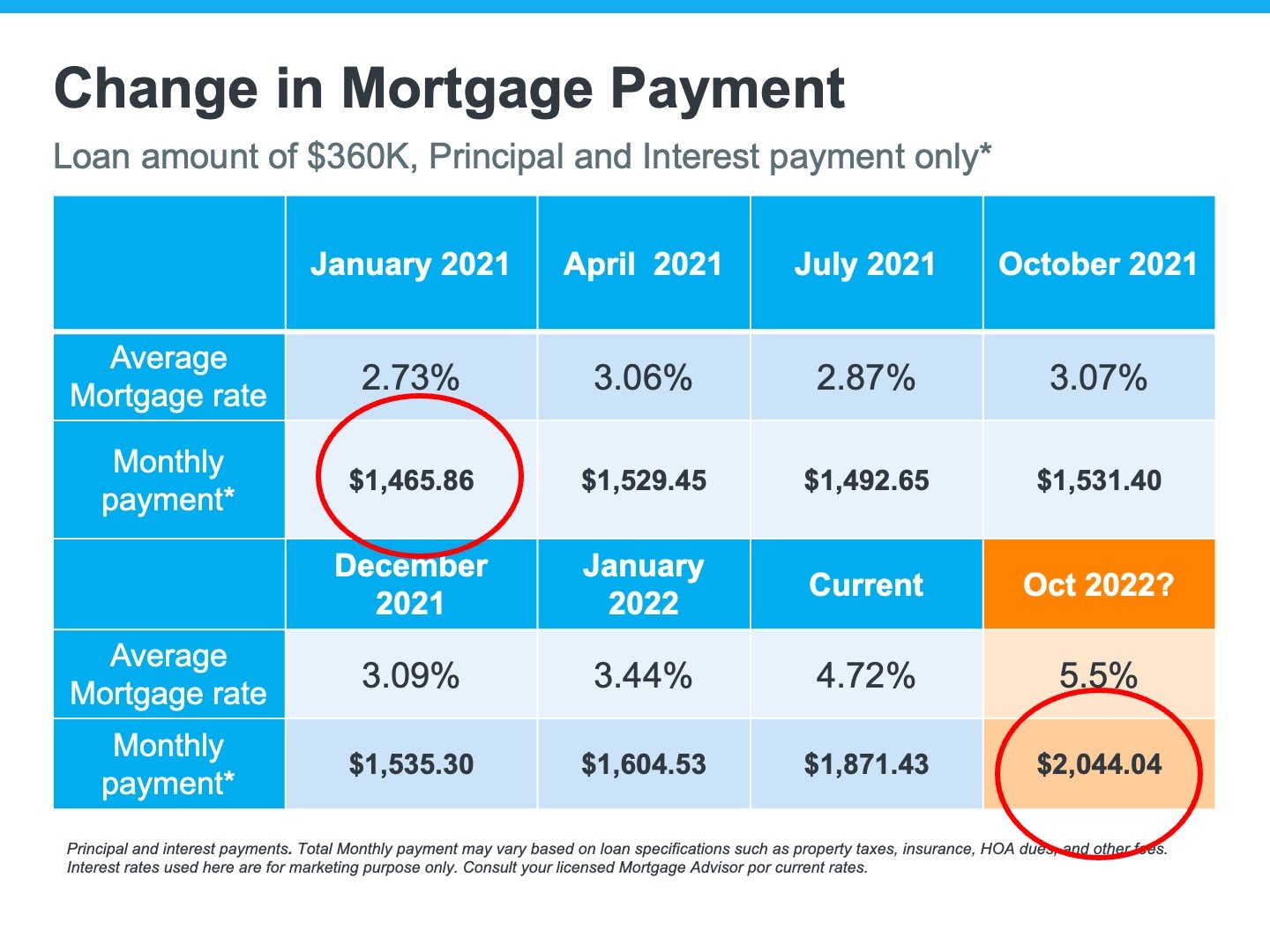

We are already starting to see the impact of rising home prices and mortgage rates on home affordability;

Typically, lenders don’t want to see the principle and interest portion of your mortgage payment exceed 28% of your income. Even with rising home prices, in the 3rd quarter of 2021 mortgage payments were only averaging 22.4% of income.

In just a few short months, that number has jumped to 29.1%, meaning some buyers will no longer qualify for as high of a purchase price and some buyers will no longer qualify at all.

Here is an example of how rising mortgage rates impact your monthly mortgage payment;

Using a $360,000 loan amount as an example, in January 2021 your monthly principal and interest payment would have been just under $1,500 per month.

Assuming mortgage rates reach 5.5% in the coming months, the mortgage payment on that same loan amount will be almost $580 higher at $2044…Ouch!!

While there are currently no indications home prices will fall in the next year or so, there is definitely a great deal of uncertainty about the economy overall.

Without a doubt, buyer demand will be impacted by rising mortgage rates and inflation. Sellers, who have been reluctant to list their homes for sale considering there hasn’t been anywhere to move to after they sell, will start coming back to the market as they start to sense things might be slowing down.

As supply increases and demand softens, I expect we’ll see market conditions start to return to normal, meaning fewer bidding wars, fewer offers, longer days on market, and moderating price appreciation.

Then again, I don’t know of anyone with a perfectly clear crystal ball. Just a few months ago it was widely believed mortgage rates wouldn’t reach 3.75% until the end of the year. Now, with the highest mortgage rates of the past decade, we are wondering just how high they might go.

Edward Seiler, AVP Housing Economics of the Mortgage Bankers Association said it best;

Each week I see several reports and videos forecasting what the housing market is going to do over the next few months, but the truth is, as Edward said, nobody really knows.

Will inflation moderate?

Will mortgage rates surpass 6%?

Will the economy experience a recession later this year?

What I do know for certain is that I bring you the latest, most up-to-date, information each and every week. As we move forward, each market across the country will be impacted differently. Here in Frisco, TX we currently have one of the hottest real estate markets in the country, and the population is expected to continue growing over the next 5 to 10 years meaning we will continue to see higher than average demand.

For the latest market conditions, check out our Frisco Market Report. From this report, you can look up current conditions for any zip code, or city, in the country with information that is updated weekly.

I also invite you to Subscribe to my YouTube Channel for additional updates and insights on the latest real estate news.

Do you have additional questions or a specific situation you’d like to discuss in more detail? Give us a call at 469-296-5230 or email Contact@S2RealEstateTeam.com